|

EXXONMOBIL

2014

EXECUTIVE

COMPENSATION

OVERVIEW

WEBINAR

2

Forward-Looking

Statements

Statements

regarding

future

events

or

conditions

are

forward-looking

statements.

Actual

future

results,

including

project

plans,

schedules,

and

results,

as

well

as

the

impact

of compensation incentives, could differ materially due to changes in oil and gas prices and

other factors affecting our industry, technical or operating conditions, and other

factors

described

under

the

heading

“Factors

Affecting

Future

Results”

in our

most

recent

Form

10-K

and

on

the

“Investors”

page at

our

website

at

exxonmobil.com.

Financial and Operating Terms

This presentation includes certain non-GAAP financial measures, including Return on Average

Capital Employed, Free Cash Flow, and Cash from Operations and Asset Sales.

For

definitions

of

and

additional

information

concerning

these

terms,

including

information

required

by

SEC

Regulation

G,

see

the

“Frequently

Used

Terms”

on

the

“Investors”

page of our website at exxonmobil.com. References in this report to oil-equivalent

barrels, resources, and similar terms may include quantities of oil and gas that are not

yet classified as proved reserves under SEC definitions but that we believe will ultimately be developed and moved into the proved reserve category. The term

“project”

as used in this presentation may refer to a variety of different activities and does not

necessarily have the same meaning as under any government payment transparency

reports. Compensation-Related Terms

Reported

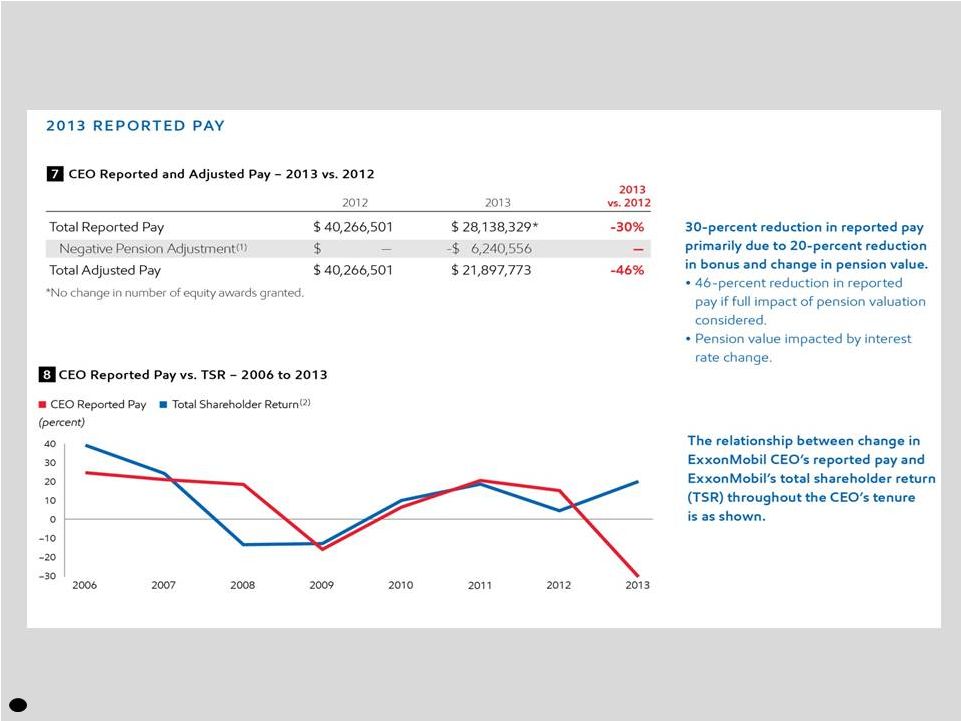

Pay

is

Total

Compensation

reported

in

the

Summary

Compensation

Table,

except

for

years

2006

to

2008,

where

the

grant

date

value

of

restricted

stock

as

provided

under

current

SEC

rules

is

used

to

put

all

years

of

compensation on the

same

basis.

Realized

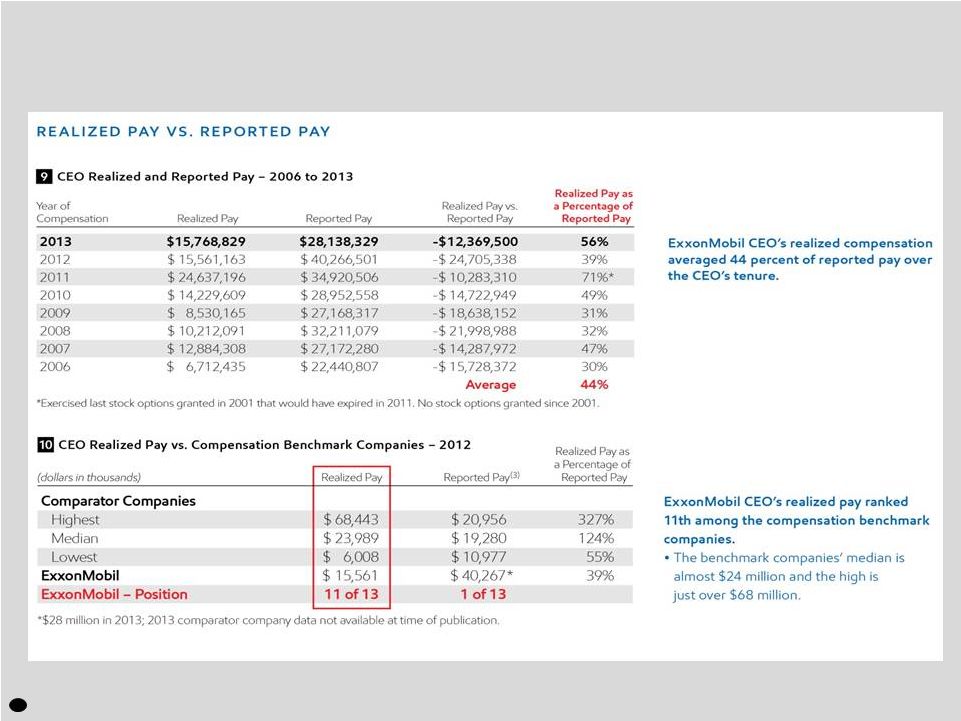

Pay

is

compensation

actually

received

by

the

CEO

during

the

year,

including

salary,

current

bonus,

payouts

of

previously

granted

Earnings

Bonus

Units

(EBU),

net

spread

on

stock

option

exercises,

market

value

at

vesting

of

previously

granted

stock-based

awards,

and

All

Other

Compensation

amounts

realized

during the

year.

It

excludes

unvested

grants,

change

in

pension

value,

and

other

amounts

that

will

not

actually

be

received

until

a

future

date.

Amounts

for

other

companies

include

salary,

bonus,

payouts

of non-equity incentive plan compensation, and All Other Compensation as reported in the

Summary Compensation Table, plus value realized on option exercise or stock vesting as

reported in the Option Exercises and Stock Vested table. It excludes unvested grants, change in pension value, and other amounts that will not actually be received

until a future date, as well as any retirement-related payouts from pension or nonqualified

compensation plans. Unrealized

Pay

includes

the

value

based

on

each

compensation

benchmark

company’s

closing

stock

price

at

fiscal

year-end

2013

of:

unvested

restricted

stock

awards;

unvested

long-term

share

and

cash

performance

awards

valued

at

target

levels;

and

the

“in

the

money”

value

of

unexercised

stock

options

(both

vested

and

unvested),

in

each

case for awards granted during the covered period. If a CEO retired during the period,

outstanding equity is included assuming that unvested awards, as of the retirement date,

continued to vest pursuant to the original terms of the award.

Compensation

Benchmark

Companies

consist

of:

AT&T,

Boeing,

Caterpillar,

Chevron,

Ford,

General

Electric,

IBM,

Johnson

&

Johnson,

Pfizer,

Procter

&

Gamble,

United

Technologies, and Verizon.

Cautionary Statement and Definitions |