Exhibit 99.2

2014 Analyst Meeting

New York Stock Exchange

March 5, 2014

Exxon Mobil

Energy lives hereTM

Cautionary Statement

“ Forward-Looking Statements. Outlooks, projections, estimates, targets, business plans, and other statements of future events or conditions in this presentation or the subsequent discussion period are forward-looking statements. Actual future results, including financial and operating performance; demand growth and mix; ExxonMobil’s production growth and mix; the amount and mix of capital expenditures; future distributions; resource additions and recoveries; finding and development costs; project plans, timing, costs, and capacities; efficiency gains; cost efficiencies; integration benefits; product sales and mix; and the impact of technology could differ materially due to a number of factors. These include changes in oil or gas prices or other market conditions affecting the oil, gas, and petrochemical industries; reservoir performance; timely completion of development projects; war and other political or security disturbances; changes in law or government regulation; the outcome of commercial negotiations; the actions of competitors and customers; unexpected technological developments; the occurrence and duration of economic recessions; unforeseen technical difficulties; and other factors discussed here and under the heading “Factors Affecting Future Results” in the Investors section of our Web site at exxonmobil.com. See also Item 1A of ExxonMobil’s 2013 Form 10-K. Forward-looking statements are based on management’s knowledge and reasonable expectations on the date hereof, and we assume no duty to update these statements as of any future date.

“ Frequently Used Terms. References to resources, resource base, recoverable resources, and similar terms include quantities of oil and gas that are not yet classified as proved reserves but that we believe will likely be moved into the proved reserves category and produced in the future. “Proved reserves” in this presentation are presented using the SEC pricing basis in effect for the year presented, except for the calculation of 20 straight years of at least 100-percent replacement; oil sands and equity company reserves are included for all periods. For definitions of, and information regarding, reserves, return on average capital employed, cash flow from operations and asset sales, free cash flow, and other terms used in this presentation, including information required by SEC Regulation G, see the “Frequently Used Terms” posted on the Investors section of our Web site. The Financial and Operating Review on our Web site also shows ExxonMobil’s net interest in specific projects.

The term ‘project’ as used in this presentation can refer to a variety of different activities and does not necessarily have the same meaning as in any government payment transparency reports.

| 2 |

|

Agenda

9am Welcome

David Rosenthal, Vice President, Investor Relations and Secretary Financial & Operating Review Energy Outlook Strategic Overview Rex Tillerson, Chairman and CEO

Risk Management

Delivering Profitable Growth

Upstream Production Growth Mark Albers, Senior Vice President

Upstream Long-Term Opportunity Set Andrew Swiger, Senior Vice President Downstream & Chemical Mike Dolan, Senior Vice President Break Summary Rex Tillerson, Chairman and CEO 11am Q&A

12pm Meeting Concludes

| 3 |

|

Financial & Operating Review

Rex Tillerson

Chairman and CEO

Financial & Operating Review

Key Messages

Maintaining relentless focus on risk management and operational excellence

Major project start-ups delivering production volume growth through 2017

Improving Upstream unit profitability

Developing a unique and balanced set of profitable growth opportunities

Continuing disciplined capital allocation

Growing free cash flow and generating long-term shareholder value

| 5 |

|

Financial & Operating Review

2013 Results

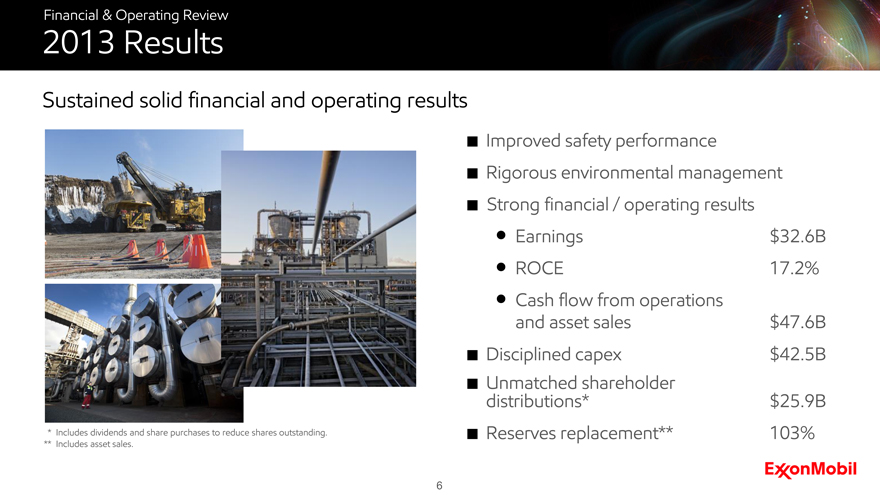

Sustained solid financial and operating results

Improved safety performance

Rigorous environmental management

Strong financial / operating results

Earnings

$32.6B

ROCE

17.2%

Cash flow from operations

| * |

|

Includes dividends and share purchases to reduce shares outstanding. and asset sales |

** Includes asset sales.

| 6 |

|

Disciplined capex

$47.6B

Unmatched shareholder distributions*

$42.5B

$25.9B

Reserves replacement**

103%

Financial & Operating Review

Safety Performance

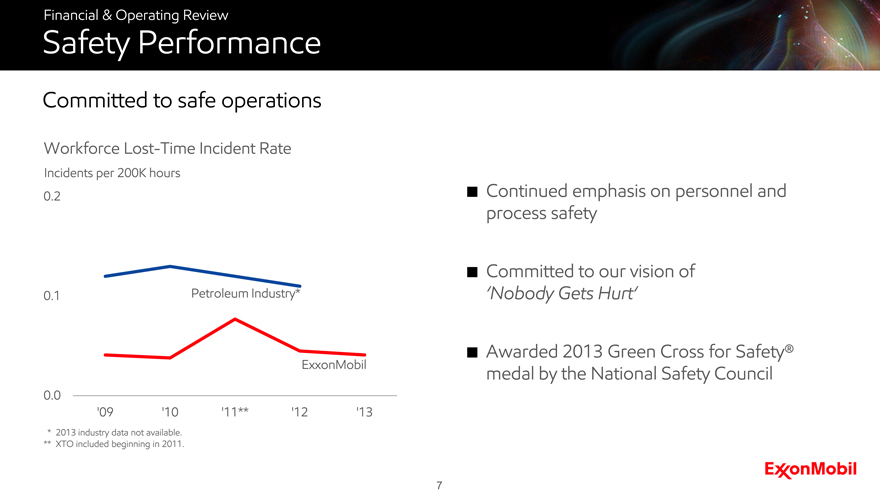

Committed to safe operations

Workforce Lost-Time Incident Rate

Incidents per 200K hours

Continued emphasis on personnel and process safety

Committed to our vision of

‘Nobody Gets Hurt’

Awarded 2013 Green Cross for Safety® medal by the National Safety Council

| * |

|

2013 industry data not available. |

** XTO included beginning in 2011.

| 7 |

|

Petroleum Industry*

ExxonMobil’09 ‘10 ‘11** ‘12 ‘13

Financial & Operating Review

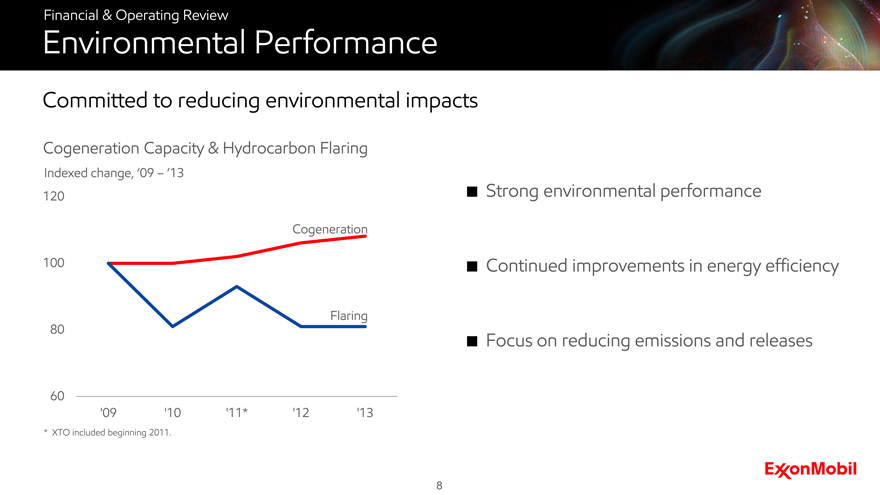

Environmental Performance

Committed to reducing environmental impacts

Cogeneration Capacity & Hydrocarbon Flaring

Indexed change, ‘09 -’13

‘09 ‘10 ‘11* ‘12 ‘13

| * |

|

XTO included beginning 2011. |

Cogeneration Flaring 120 100 80 60

Strong environmental performance

Continued improvements in energy efficiency

Focus on reducing emissions and releases

| 8 |

|

Financial & Operating Review

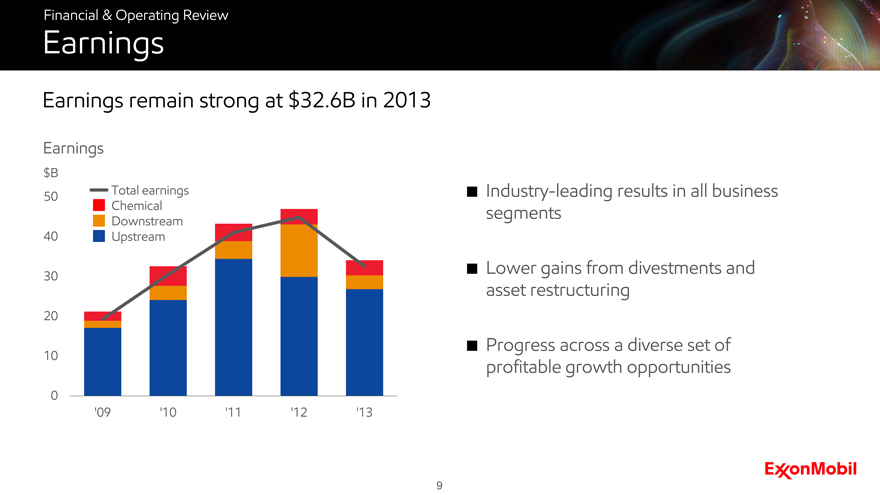

Earnings

Earnings remain strong at $32.6B in 2013

Earnings

$B

50 40

30 20 10 0 ‘09 ‘10 ‘11 ‘12 ‘13

Total earnings

Chemical

Downstream

Upstream

Industry-leading results in all business segments

Lower gains from divestments and asset restructuring

Progress across a diverse set of profitable growth opportunities

| 9 |

|

Financial & Operating Review

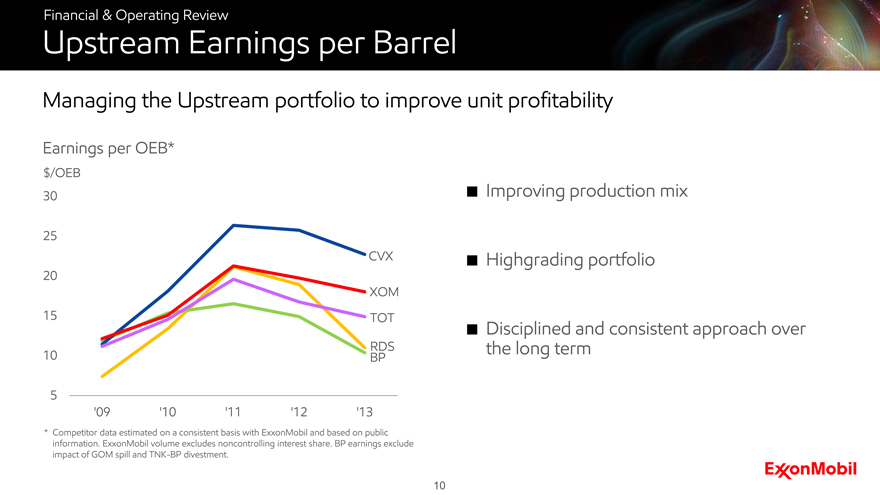

Upstream Earnings per Barrel

Managing the Upstream portfolio to improve unit profitability

Earnings per OEB*

$/OEB

30 25 20 15 10 5 ‘09 ‘10 ‘11 ‘12 ‘13

CVX XOM TOT RDS BP

* Competitor data estimated on a consistent basis with ExxonMobil and based on public information. ExxonMobil volume excludes noncontrolling interest share. BP earnings exclude impact of GOM spill and TNK-BP divestment.

Improving production mix

Highgrading portfolio

Disciplined and consistent approach over the long term

10

Financial & Operating Review

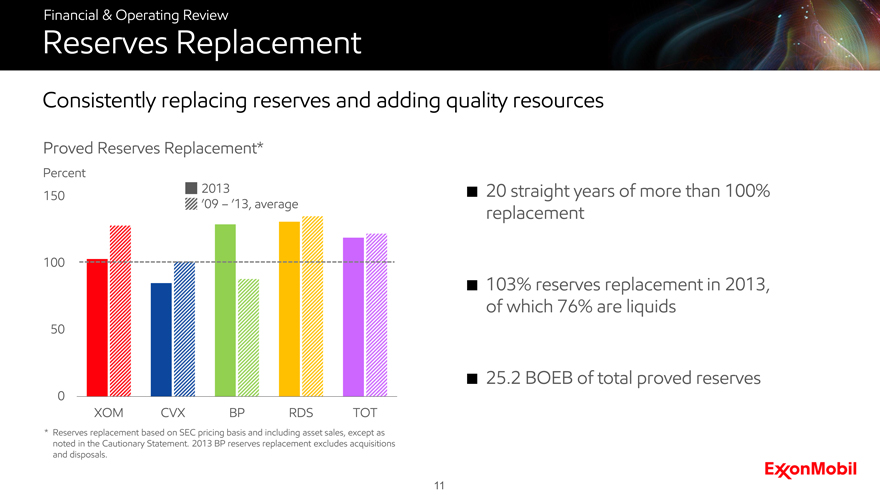

Reserves Replacement

Consistently replacing reserves and adding quality resources

Proved Reserves Replacement*

Percent

* Reserves replacement based on SEC pricing basis and including asset sales, except as noted in the Cautionary Statement. 2013 BP reserves replacement excludes acquisitions and disposals.

20 straight years of more than 100% replacement

103% reserves replacement in 2013, of which 76% are liquids

25.2 BOEB of total proved reserves

11

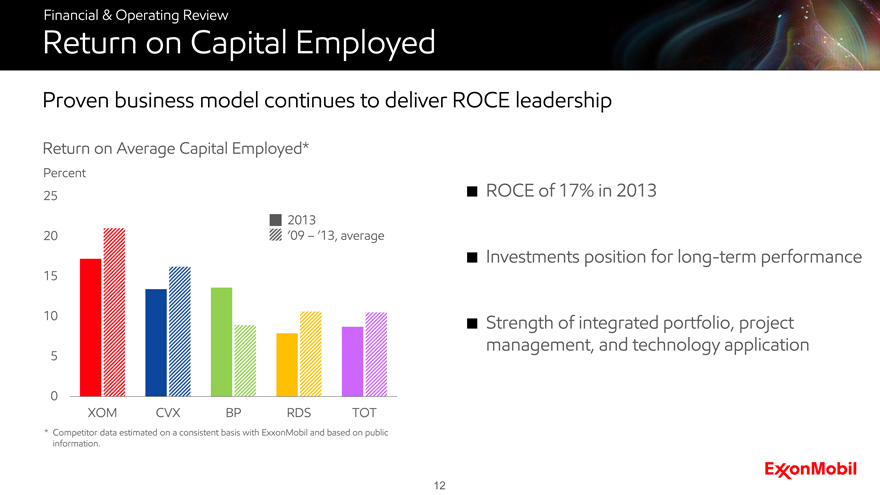

Financial & Operating Review

Return on Capital Employed

Proven business model continues to deliver ROCE leadership

Return on Average Capital Employed*

Percent

| * |

|

Competitor data estimated on a consistent basis with ExxonMobil and based on public information. |

ROCE of 17% in 2013

Investments position for long-term performance

Strength of integrated portfolio, project management, and technology application

12

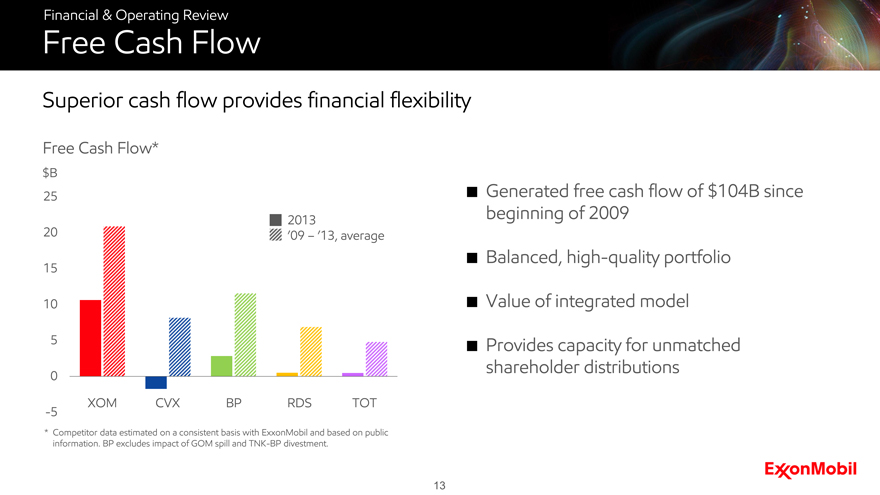

Financial & Operating Review

Free Cash Flow

Superior cash flow provides financial flexibility

Free Cash Flow*

$B

XOM CVX BP RDS TOT

Generated free cash flow of $104B since beginning of 2009

Balanced, high-quality portfolio

Value of integrated model

Provides capacity for unmatched shareholder distributions

* Competitor data estimated on a consistent basis with ExxonMobil and based on public information. BP excludes impact of GOM spill and TNK-BP divestment.

$B 25 20 15 10 5 0 -5 XOM CVX BP RDS TOT 2013 ‘09- ‘13, average

13

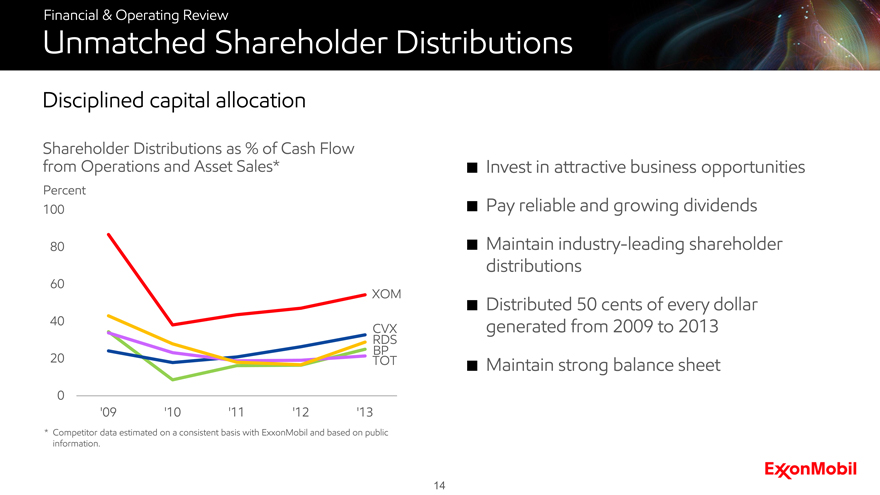

Financial & Operating Review

Unmatched Shareholder Distributions

Disciplined capital allocation

Shareholder Distributions as % of Cash Flow from Operations and Asset Sales*

Percent

| * |

|

Competitor data estimated on a consistent basis with ExxonMobil and based on public information. |

Invest in attractive business opportunities

Pay reliable and growing dividends

Maintain industry-leading shareholder distributions

Distributed 50 cents of every dollar generated from 2009 to 2013

Maintain strong balance sheet

14

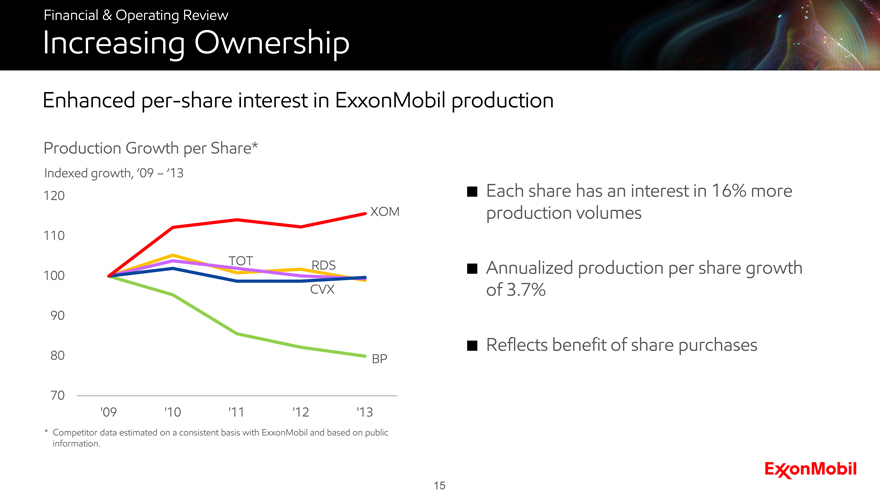

Financial & Operating Review

Increasing Ownership

Enhanced per-share interest in ExxonMobil production

Production Growth per Share*

Indexed growth, ‘09 - ‘13

| * |

|

Competitor data estimated on a consistent basis with ExxonMobil and based on public information. |

Each share has an interest in 16% more production volumes

Annualized production per share growth of 3.7%

Reflects benefit of share purchases

120 110 100 90 80 70 ‘09 ‘10 ‘11 ‘12 ‘13 BP CVX RDS TOT XOM

15

Financial & Operating Review

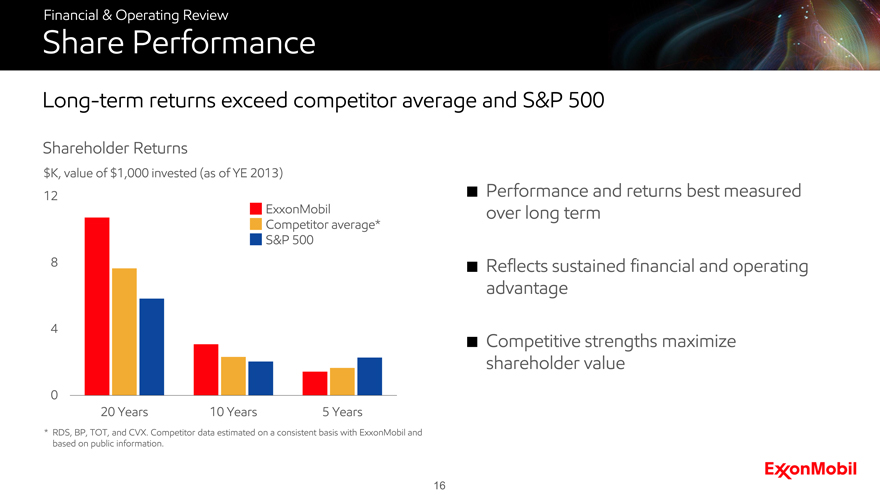

Share Performance

Long-term returns exceed competitor average and S&P 500

Shareholder Returns

$K, value of $1,000 invested (as of YE 2013)

ExxonMobil Competitor average* S&P 500

* RDS, BP, TOT, and CVX. Competitor data estimated on a consistent basis with ExxonMobil and based on public information.

Performance and returns best measured over long term

Reflects sustained financial and operating advantage

Competitive strengths maximize shareholder value

12 8 4 0 20 Years 10 Years 5 Years

16

Energy Outlook

Rex Tillerson

Chairman and CEO

Energy Outlook

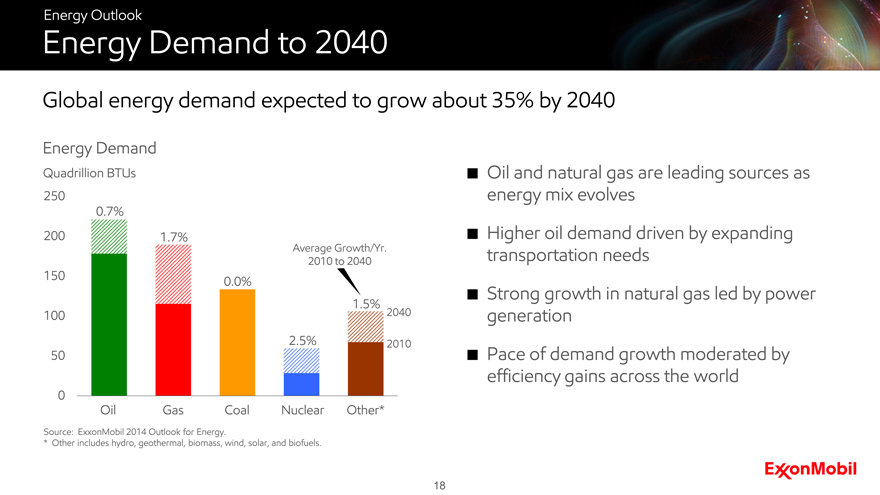

Energy Demand to 2040

Global energy demand expected to grow about 35% by 2040

Energy Demand

Quadrillion BTUs Oil and natural gas are leading sources as energy mix evolves

Higher oil demand driven by expanding transportation needs

Strong growth in natural gas led by power generation

Pace of demand growth moderated by efficiency gains across the world

Source: ExxonMobil 2014 Outlook for Energy.

| * |

|

Other includes hydro, geothermal, biomass, wind, solar, and biofuels. |

250 200 150 100 50 0 Oil Gas Coal Nuclear Other* 0.7% 1.7% 0.0% 2.5% 1.5% 2040 2010

Average Growth/Yr. 2010 to 2040

18

Energy Outlook

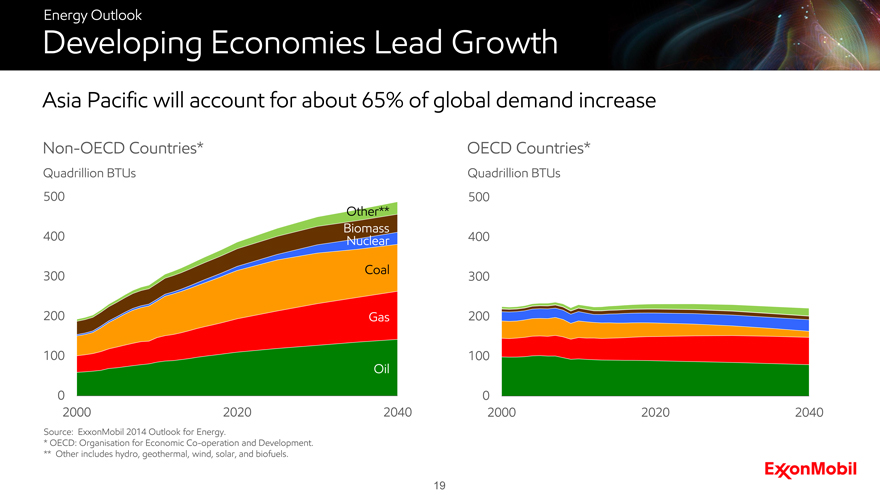

Developing Economies Lead Growth

Asia Pacific will account for about 65% of global demand increase

Non-OECD Countries* OECD Countries*

Quadrillion BTUs Quadrillion BTUs

Source: ExxonMobil 2014 Outlook for Energy.

| * |

|

OECD: Organisation for Economic Co-operation and Development. |

** Other includes hydro, geothermal, wind, solar, and biofuels.

19

Energy Outlook

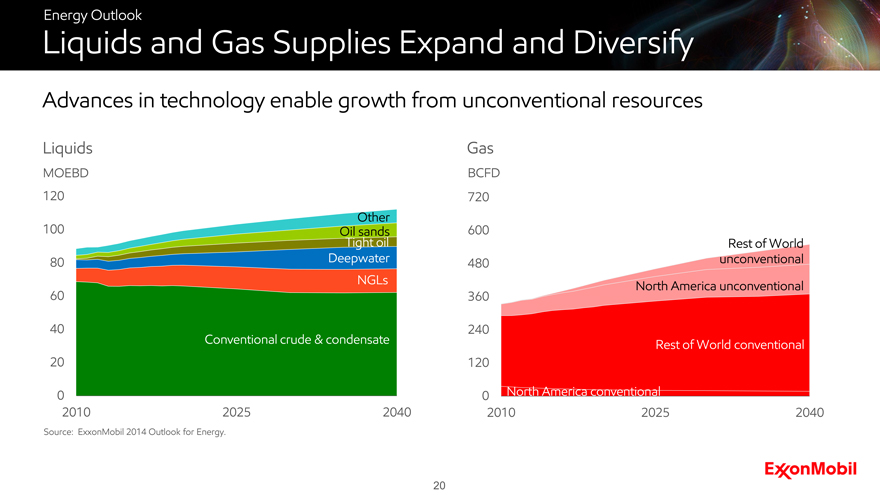

Liquids and Gas Supplies Expand and Diversify

Advances in technology enable growth from unconventional resources

Liquids Gas

MOEBD BCFD

Source: ExxonMobil 2014 Outlook for Energy.

120 100 80 60 40 20 0 2010 2025 2040

Others Oil sands Tight oil Deepwater NGLs Conventional crude & condensate

720 600 480 360 240 120 0 2010 2025 2040

Rest of World unconventional North America unconventional Rest of World conventional North America conventional

20

Energy Outlook

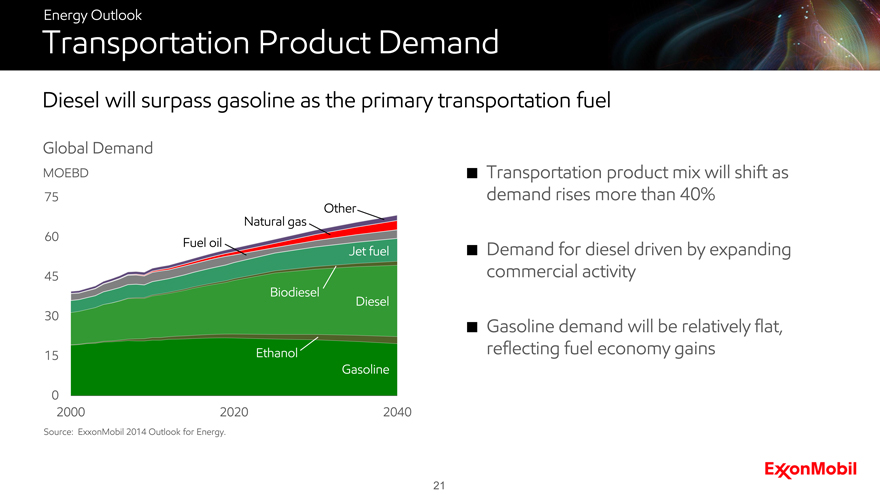

Transportation Product Demand

Diesel will surpass gasoline as the primary transportation fuel

Global Demand

MOEBD Transportation product mix will shift as demand rises more than 40%

Demand for diesel driven by expanding commercial activity

Gasoline demand will be relatively flat, reflecting fuel economy gains

Source: ExxonMobil 2014 Outlook for Energy.

75 60 45 30 15 0 2000 2020 2040

Biodiesel Ethanol Gasoline Diesel Jet fuel Fuel oil Natural gas Other

21

Energy Outlook

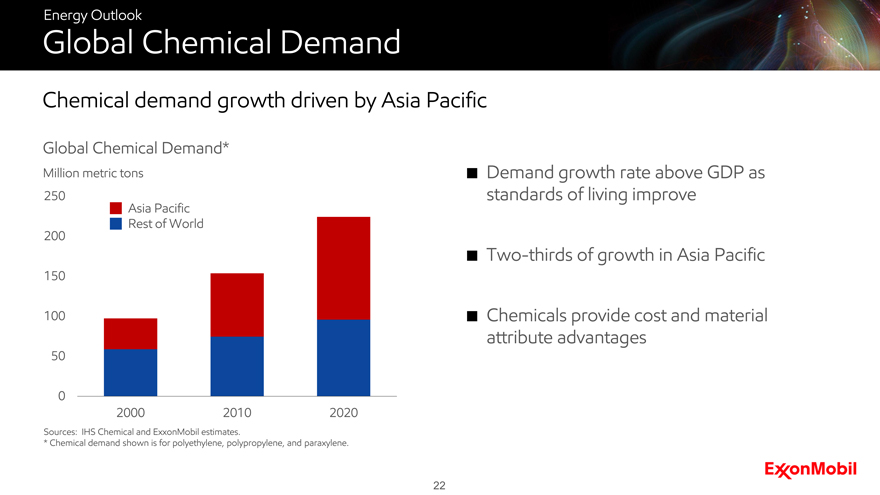

Global Chemical Demand

Chemical demand growth driven by Asia Pacific

Global Chemical Demand*

Million metric tons Demand growth rate above GDP as standards of living improve

Two-thirds of growth in Asia Pacific

Chemicals provide cost and material attribute advantages

Sources: IHS Chemical and ExxonMobil estimates.

| * |

|

Chemical demand shown is for polyethylene, polypropylene, and paraxylene. |

250 200 150 100 50 0 2000 2010 2020

Asia Pacific Rest of World

22

Energy Outlook

Key Perspectives

Outlook guides our business strategy and investment plans

Development of practical, reliable and affordable energy remains paramount

Access to high-quality resources both necessary and challenging

Technology advancements are key enabler to safe and effective development

Substantial investments are required to meet growing demand

Free trade and sound, stable government policies are vital

Long-term investment planning and near-term execution are imperative

23

Strategic Overview

Rex Tillerson

Chairman and CEO

Strategic Overview

Key Elements of ExxonMobil Strategy

Unrelenting focus on creating long-term shareholder value

Employ effective risk management and lead industry in operational excellence

Manage a diversified, balanced portfolio to mitigate risks and optimize profitability

Leverage integration benefits

Select and execute the most attractive investment opportunities

Develop and utilize advanced technologies

Attract and retain a talented, diverse workforce

Deliver superior, long-term total returns to shareholders

25

Risk Management

Rex Tillerson

Chairman and CEO

Risk Management

Risk management is at the core of our business

Operations Integrity Management System (OIMS)

Systematic managed approach

Rigorously applied systems and processes

Clearly defined policies, standards and practices Ensure accountability Measure performance Recognize progress

Plan future improvements

27

Risk Management

Incident Prevention & Emergency Preparedness

Leveraging proven systems

Comprehensive risk assessment protocols

Sound design, construction, operating and maintenance standards

Continuous inspection and state-of-the-art process control systems

Fully integrated incident command system

Well-trained emergency response teams

28

Delivering Profitable Growth

Rex Tillerson

Chairman and CEO

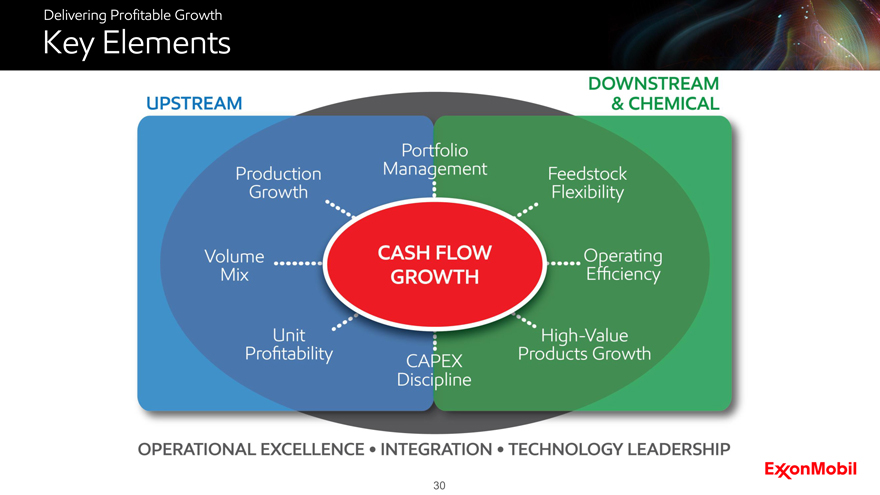

Delivering Profitable Growth

Key Elements

30

Delivering Profitable Growth

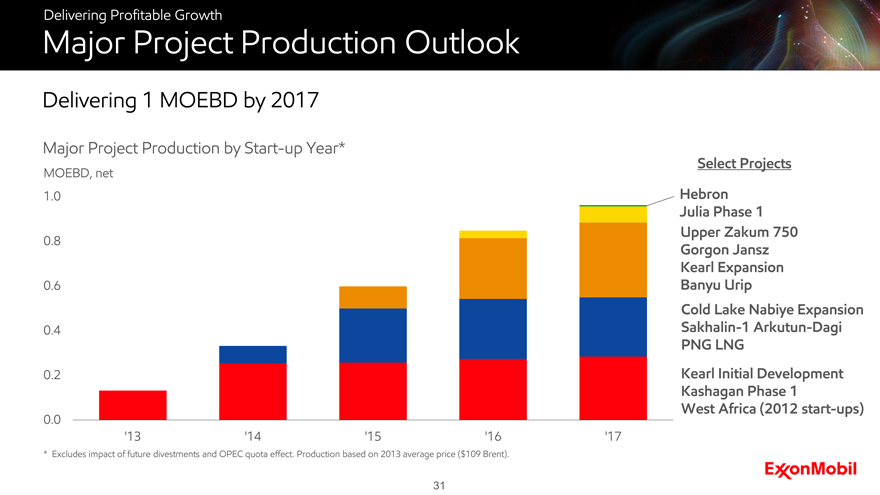

Major Project Production Outlook

Delivering 1 MOEBD by 2017

Major Project Production by Start-up Year*

MOEBD, net

1.0 0.8 0.6 0.4 0.2 0.0

‘13 ‘14 ‘15 ‘16 ‘17

Select Projects

Hebron Julia Phase 1 Upper Zakum 750 Gorgon Jansz

Kearl Expansion Banyu Urip

Cold Lake Nabiye Expansion Sakhalin-1 Arkutun-Dagi

PNG LNG

Kearl Initial Development Kashagan Phase 1

West Africa (2012 start-ups)

| * |

|

Excludes impact of future divestments and OPEC quota effect. Production based on 2013 average price ($109 Brent). |

31

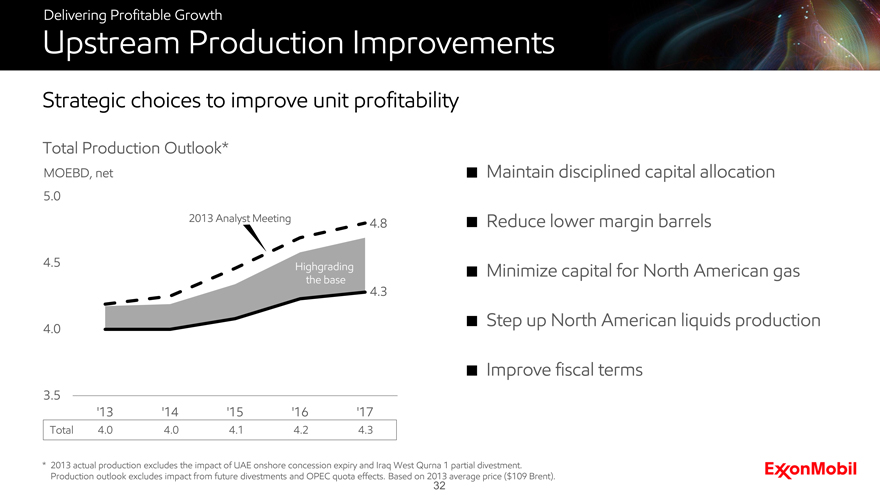

Delivering Profitable Growth

Upstream Production Improvements

Strategic choices to improve unit profitability

Total Production Outlook*

MOEBD, net

Highgrading the base

Maintain disciplined capital allocation

Reduce lower margin barrels

Minimize capital for North American gas

Step up North American liquids production

Improve fiscal terms

* 2013 actual production excludes the impact of UAE onshore concession expiry and Iraq West Qurna 1 partial divestment. Production outlook excludes impact from future divestments and OPEC quota effects. Based on 2013 average price ($109 Brent).

5.0 4.5 4.0 3.5 ‘13 ‘14 ‘15 ‘16 ‘17

Total 4.0 4.0 4.1 4.2 4.3

2013 Analyst Meeting 4.8 4.3

32

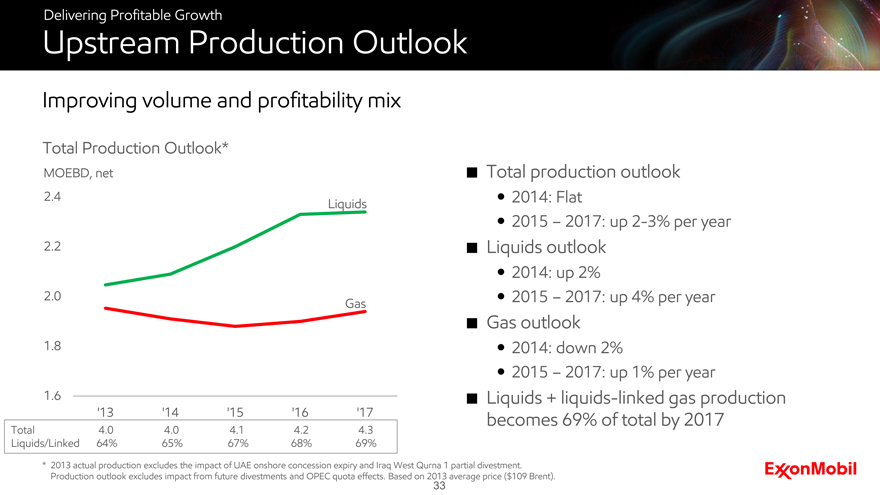

Delivering Profitable Growth

Upstream Production Outlook

Improving volume and profitability mix

Total Production Outlook*

MOEBD, net Total production outlook

2014: Flat

2015 _ 2017: up 2-3% per year

Liquids outlook

2014: up 2%

2015 _ 2017: up 4% per year

Gas outlook

2014: down 2%

2015 _ 2017: up 1% per year

Liquids + liquids-linked gas production becomes 69% of total by 2017

* 2013 actual production excludes the impact of UAE onshore concession expiry and Iraq West Qurna 1 partial divestment. Production outlook excludes impact from future divestments and OPEC quota effects. Based on 2013 average price ($109 Brent).

Total Production Outlook* MOEBD, net

2.4 2.2 1.8 1.6 ,13 ,14 ,15 ,16 ,17

Total 4.0 4.0 4.1 4.2 4.3

Liquids/Linked 64% 65% 67% 68% 69%

Liquids Gas

ExxonMobil

33

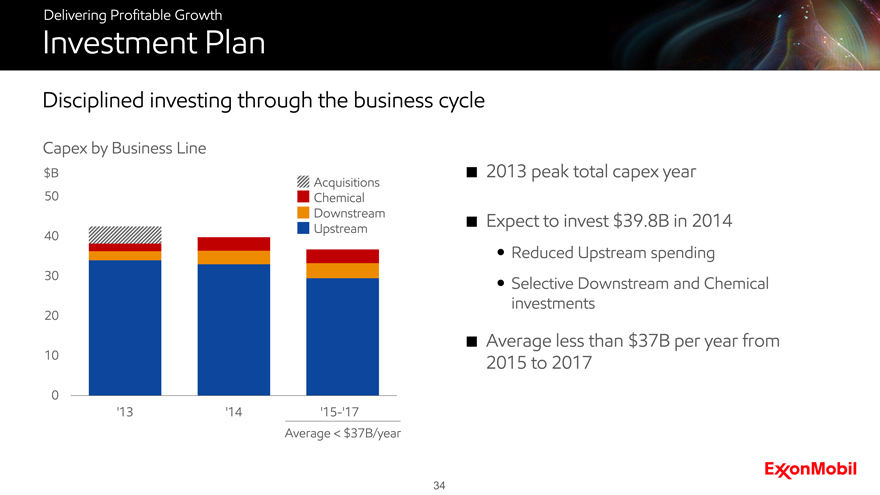

Delivering Profitable Growth

Investment Plan

Disciplined investing through the business cycle

Capex by Business Line

2013 peak total capex year

Expect to invest $39.8B in 2014

Reduced Upstream spending

Selective Downstream and Chemical investments

Average less than $37B per year from 2015 to 2017

$B 50 40 30 20 10 0 ‘13 ‘14 ‘15-’17

Acquisitions Chemical Downstream Upstream

Average < $37B/year

34

Delivering Profitable Growth

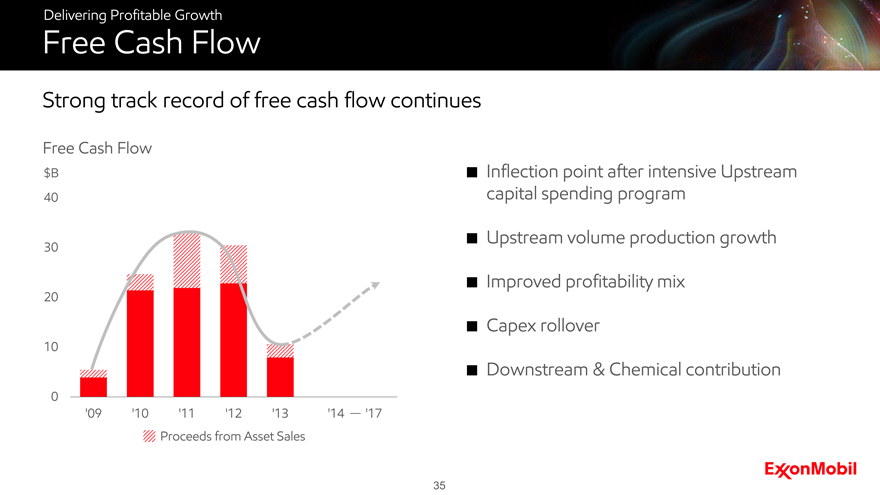

Free Cash Flow

Strong track record of free cash flow continues

Free Cash Flow

$B Inflection point after intensive Upstream capital spending program

Upstream volume production growth

Improved profitability mix

Capex rollover

Downstream & Chemical contribution

40 30 20 10 0

‘09 ‘10 ‘11 ‘12 ‘13 ‘14 - ‘17

Proceeds from Asset Sales

35

Upstream Production Growth through 2017

Mark Albers

Senior Vice President

Upstream Production Growth through 2017

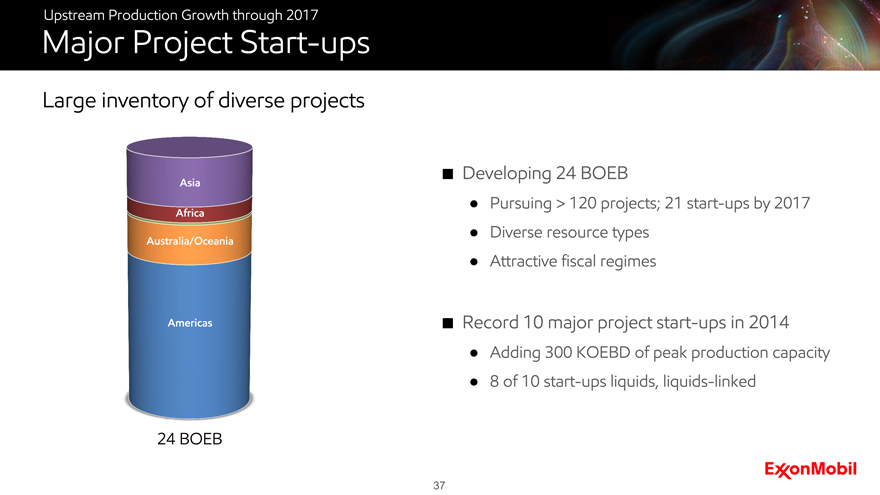

Major Project Start-ups

Large inventory of diverse projects

Asia Africa

Australia/Oceania

Americas

24 BOEB

Developing 24 BOEB

Pursuing > 120 projects; 21 start-ups by 2017

Diverse resource types

Attractive fiscal regimes

Record 10 major project start-ups in 2014

Adding 300 KOEBD of peak production capacity

8 of 10 start-ups liquids, liquids-linked

37

Upstream Production Growth through 2017

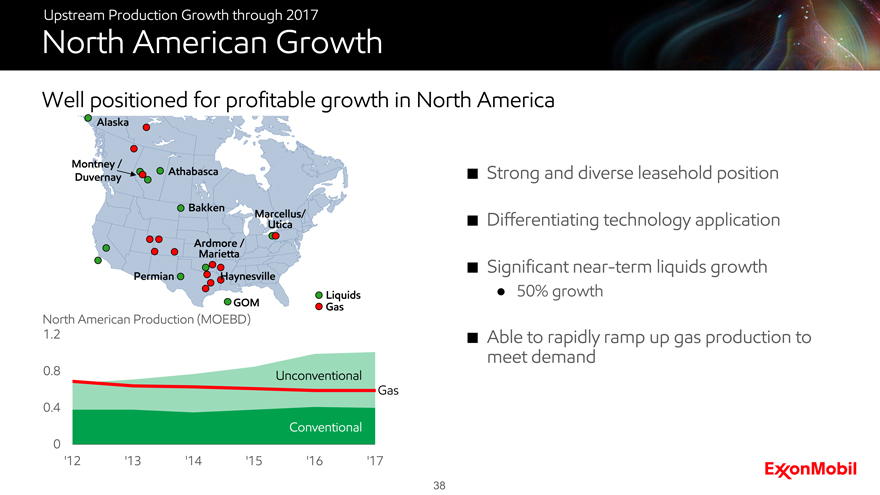

North American Growth

Well positioned for profitable growth in North America

North American Production (MOEBD)

1.2 0.8 0.4 0 ‘12 ‘13 ‘14 ‘15 ‘16 ‘17

Conventional

Unconventional Gas

Liquids

Gas

Strong and diverse leasehold position

Differentiating technology application

Significant near-term liquids growth

50% growth

Able to rapidly ramp up gas production to meet demand

38

Upstream Production Growth through 2017

US Liquids Growth

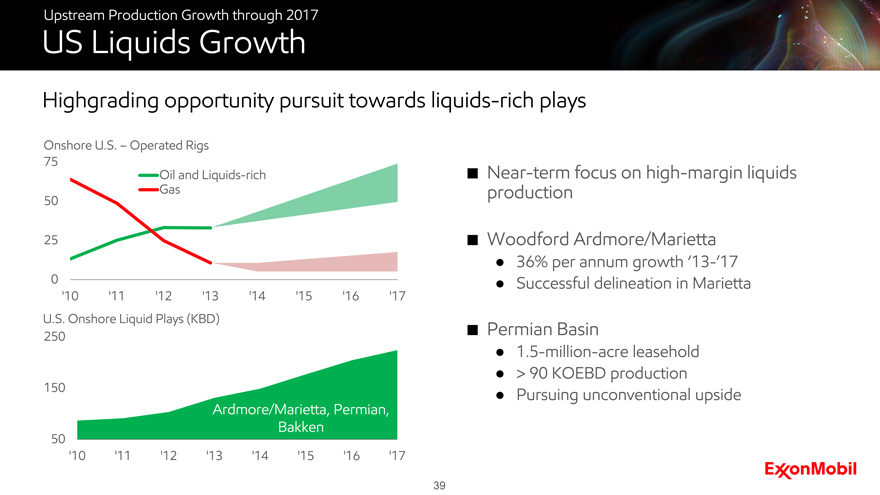

Highgrading opportunity pursuit towards liquids-rich plays

Onshore U.S. - Operated Rigs

75 50 25 0

Oil and Liquid-rich

Gas

‘10 ‘11 ‘12 ‘13 ‘14 ‘15 ‘16 ‘17

U.S. Onshore Liquid Plays (KBD)

250 150 50

Ardmore/Marietta, Permian, Bakken

‘10 ‘11 ‘12 ‘13 ‘14 ‘15 ‘16 ‘17

Near-term focus on high-margin liquids production

Woodford Ardmore/Marietta

36% per annum growth ‘13-’17

Successful delineation in Marietta

Permian Basin

1.5 -million-acre leasehold

> 90 KOEBD production

Pursuing unconventional upside

39

Upstream Production Growth through 2017

Bakken Tight Oil

Delivering high-margin growth in the Onshore U.S.

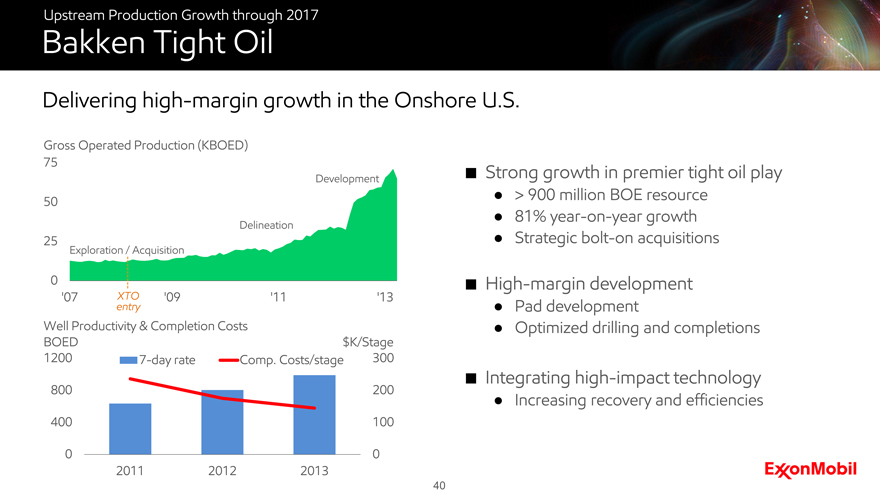

Strong growth in premier tight oil play

> 900 million BOE resource

81% year-on-year growth

Strategic bolt-on acquisitions

High-margin development

Pad development

Optimized drilling and completions

Integrating high-impact technology

Increasing recovery and efficiencies

Gross Operated Production (KBOED)

75 50 25 0 ‘07 ‘09 ‘11 ‘13 XTO entry

Well Productivity & Completion Costs

BOED 1200 800 400 0 2011 2012 2013 0 100 200 300 $K/Stage

Delineation Development

40

Upstream Production Growth through 2017

Oil Sands – Kearl Start-up

Initiated production – providing 40+ years of plateau volumes

Innovative froth treatment design creating value and driving capital efficiency

4.6 billion-barrel resource

Production steadily increasing to design capacity

Capturing benefits from “design one, build multiple” approach

Expansion project 75% complete; start-up in 4Q 2015

Future debottlenecking opportunities

Initial Development

Expansion

41

Upstream Production Growth through 2017

Oil Sands – Value Chain Integration

Leveraging full value chain to maximize profitability:

Research – Production – Logistics – Refining – Marketing

Capturing technology benefits and near-term optimization

Attractive logistic solutions that deliver broad market access

Capitalizing on North American logistics, refining, and marketing opportunities

42

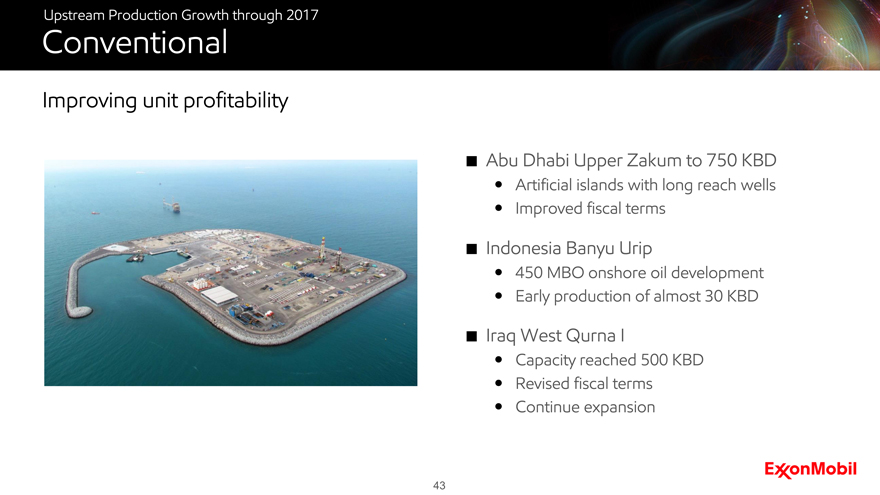

Upstream Production Growth through 2017

Conventional

Improving unit profitability

Abu Dhabi Upper Zakum to 750 KBD

Artificial islands with long reach wells Improved fiscal terms

Indonesia Banyu Urip

450 MBO onshore oil development Early production of almost 30 KBD

Iraq West Qurna I

Capacity reached 500 KBD Revised fiscal terms Continue expansion

43

Upstream Production Growth through 2017

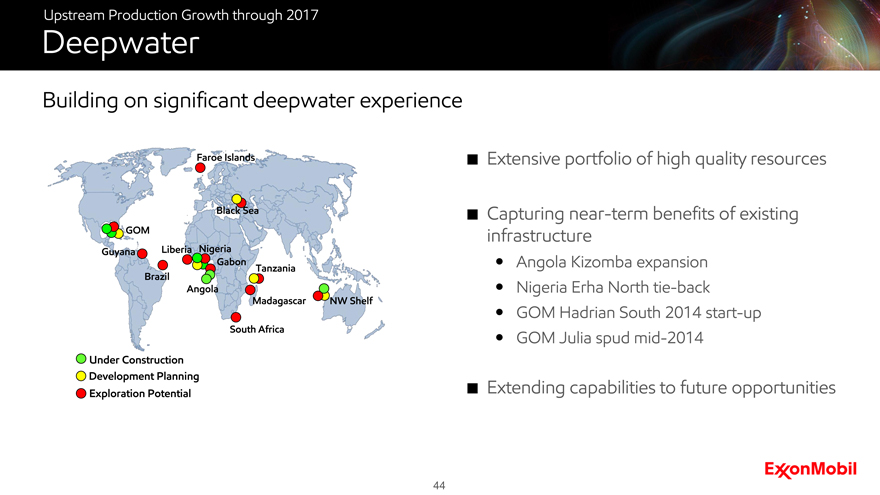

Deepwater

Building on significant deepwater experience

Extensive portfolio of high quality resources

Capturing near-term benefits of existing infrastructure

Angola Kizomba expansion Nigeria Erha North tie-back GOM Hadrian South 2014 start-up GOM Julia spud mid-2014

Extending capabilities to future opportunities

Under Construction Development Planning Exploration Potential

44

Upstream Production Growth through 2017

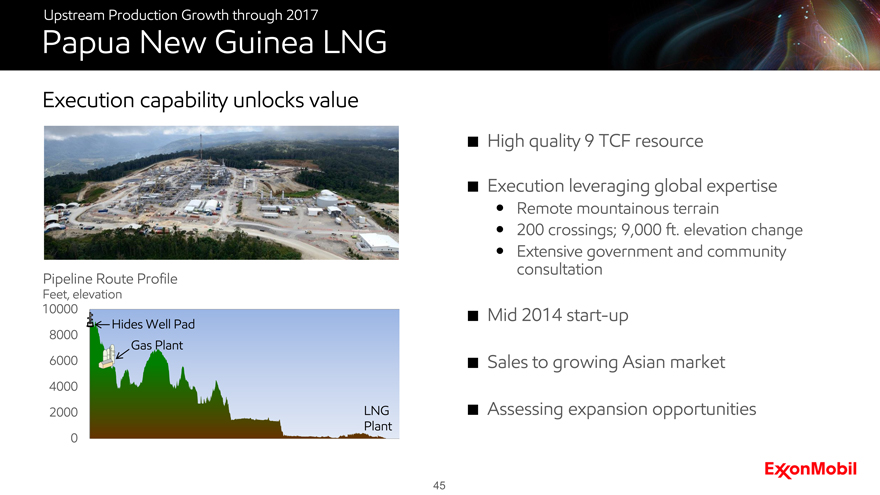

Papua New Guinea LNG

Execution capability unlocks value

High quality 9 TCF resource

Execution leveraging global expertise

Remote mountainous terrain

200 crossings; 9,000 ft. elevation change Extensive government and community consultation

Mid 2014 start-up

Sales to growing Asian market

Assessing expansion opportunities

Pipeline Route Profile

Feet, elevation

10000 8000 6000 4000 2000 0 Hides Well Pad Gas Plant LNG Plant

45

Upstream Production Growth through 2017

Arctic

Continuing more than 90 years of arctic development

Sakhalin-1 Arkutun-Dagi

Installing topsides in mid-2014 Target start-up around year-end 2014

Hebron

Gravity-based structure and topside construction underway 2017 production start-up

Hibernia Southern Extension

Extending Hibernia producing life Full project start-up in 2Q 2014

46

Upstream Production Growth through 2017

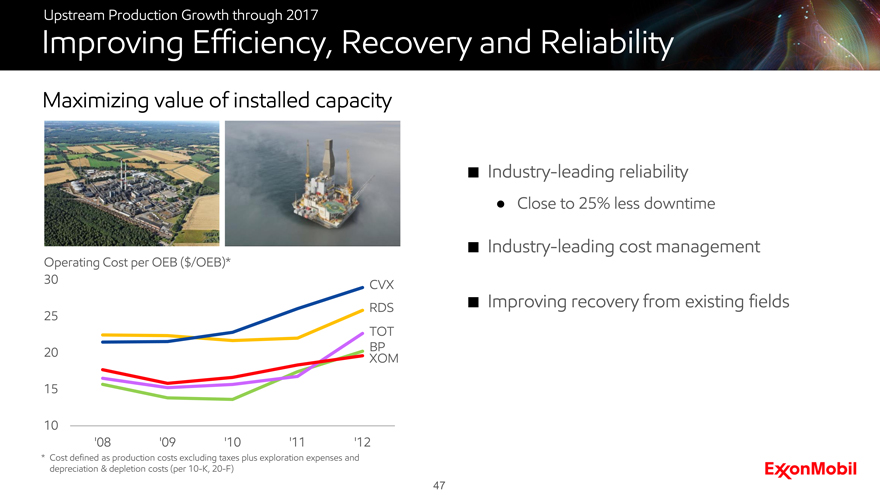

Improving Efficiency, Recovery and Reliability

Maximizing value of installed capacity

Industry-leading reliability

Close to 25% less downtime

Industry-leading cost management

Improving recovery from existing fields

* Cost defined as production costs excluding taxes plus exploration expenses and depreciation & depletion costs (per 10-K, 20-F)

Operating Cost per OEB ($/OEB)* CVX RDS TOT BP XOM

30 25 20 15 10 ‘08 ‘09 ‘10 ‘11 ‘12

47

Upstream Production Growth through 2017

Summary

Major start-ups delivering 1 MOEBD net production by 2017

Delivering profitable growth

Deep and diverse portfolio

Superior execution capability

Industry-leading technologies

Disciplined cost management

48

Upstream Long-Term Opportunity Set

Andrew Swiger

Senior Vice President

Upstream Long-Term Opportunity Set

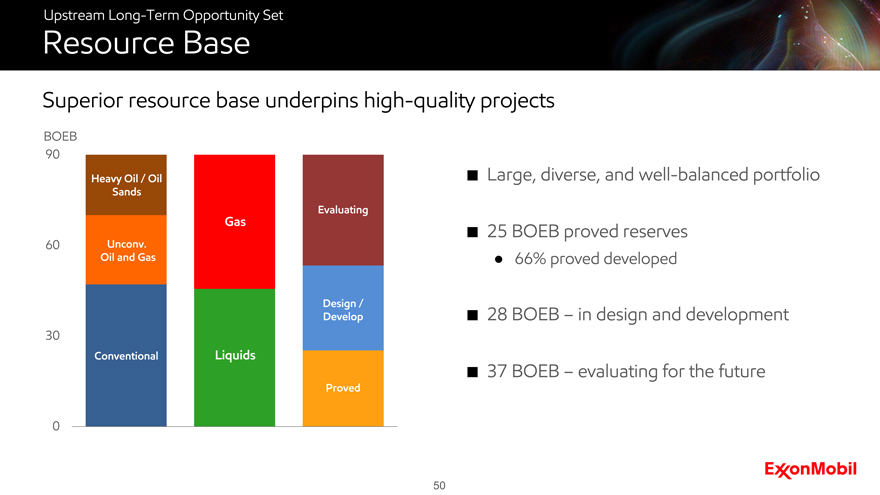

Resource Base

Superior resource base underpins high-quality projects

Large, diverse, and well-balanced portfolio

25 BOEB proved reserves

66% proved developed

28 BOEB – in design and development

37 BOEB – evaluating for the future

BOEB 90 60 30 0 Heavy Oil/ Oil Sands Uncov. Oil and Gas Conventional Gas Liquids Evaluating Design / Develop Proved

50

Upstream Long-Term Opportunity Set

New Opportunity Growth

Large portfolio of quality opportunities enables selectivity

Play Type Deepwater / Conventional Arctic Unconventional

51

Upstream Long-Term Opportunity Set

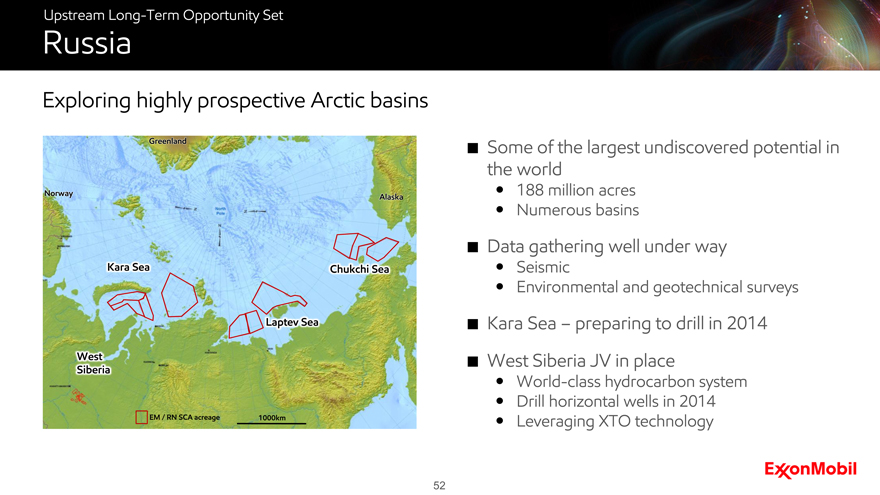

Russia

Exploring highly prospective Arctic basins

Some of the largest undiscovered potential in the world

188 million acres Numerous basins

Data gathering well under way

Seismic

Environmental and geotechnical surveys

Kara Sea - preparing to drill in 2014

West Siberia JV in place

World-class hydrocarbon system Drill horizontal wells in 2014 Leveraging XTO technology

52

Upstream Long-Term Opportunity Set

Black Sea

Strong position in emerging new hydrocarbon province

Appraising Romania Domino discovery

Multi-TCF discovery

Significant follow-on potential

Pursuing Ukraine Skifska block

Preparing to test new basin in Russia

990 thousand acres; multiple plays

Processing seismic

Plans for 2014/2015 well

53

Upstream Long-Term Opportunity Set

Kurdistan Region of Iraq

Testing large structures in proven plays

Significant hydrocarbon potential

Offset discoveries

Six PSCs; multiple plays

Acquired seismic data in 2013

Two rig operations underway

54

Upstream Long-Term Opportunity Set

Global Unconventional

Advancing potential world-class unconventional plays

Leveraging XTO capabilities

Argentina – delineating play

High-potential Vaca Muerta oil and gas shale plays

Testing under way

Colombia – commencing operations

Promising La Luna liquids potential

Canada – expanding portfolio

High-quality Clyden heavy oil leases

Celtic acquisition – delineating liquid rich plays

Near term production

55

Upstream Long-Term Opportunity Set

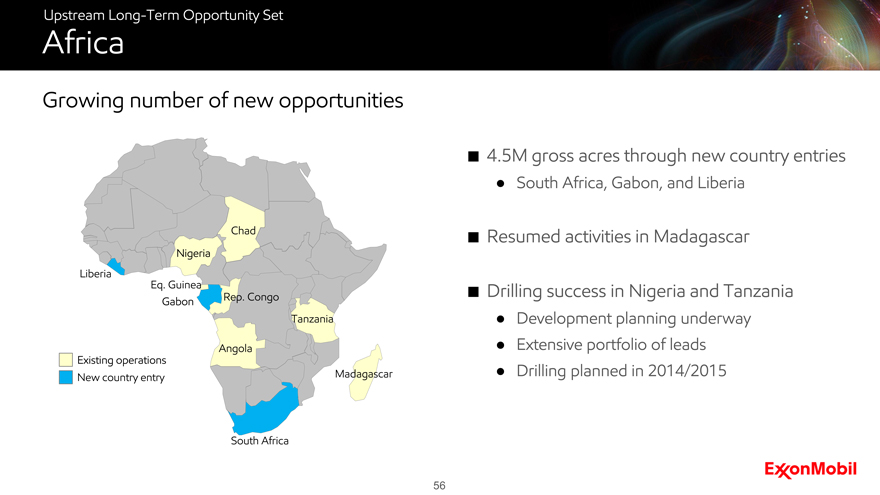

Africa

Growing number of new opportunities

4.5M gross acres through new country entries

South Africa, Gabon, and Liberia

Resumed activities in Madagascar

Drilling success in Nigeria and Tanzania

Development planning underway

Extensive portfolio of leads

Drilling planned in 2014/2015

Existing operations

New country entry

56

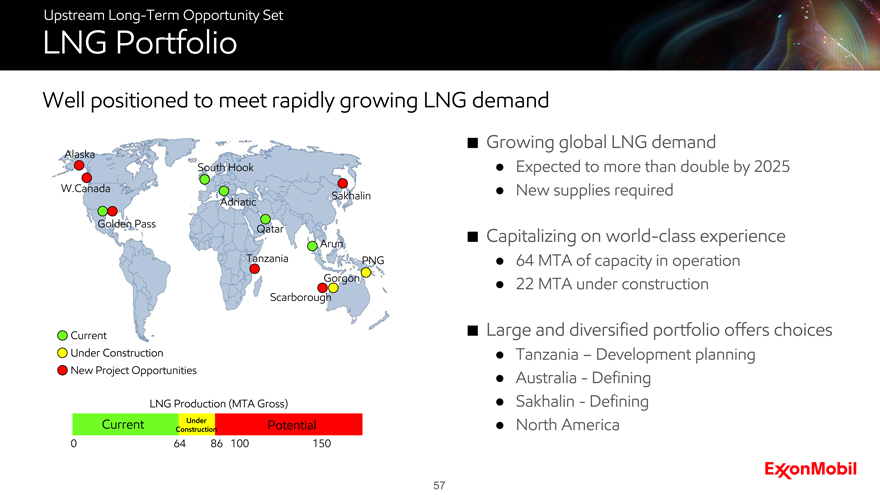

Upstream Long-Term Opportunity Set

LNG Portfolio

Well positioned to meet rapidly growing LNG demand

Under Construction

New Project Opportunities

LNG Production (MTA Gross)

Current

Under Construction

0 64 86 100 150

Growing global LNG demand

Expected to more than double by 2025

New supplies required

Capitalizing on world-class experience

64 MTA of capacity in operation

22 MTA under construction

Large and diversified portfolio offers choices

Tanzania - Development planning

Australia - Defining

Sakhalin - Defining

North America

57

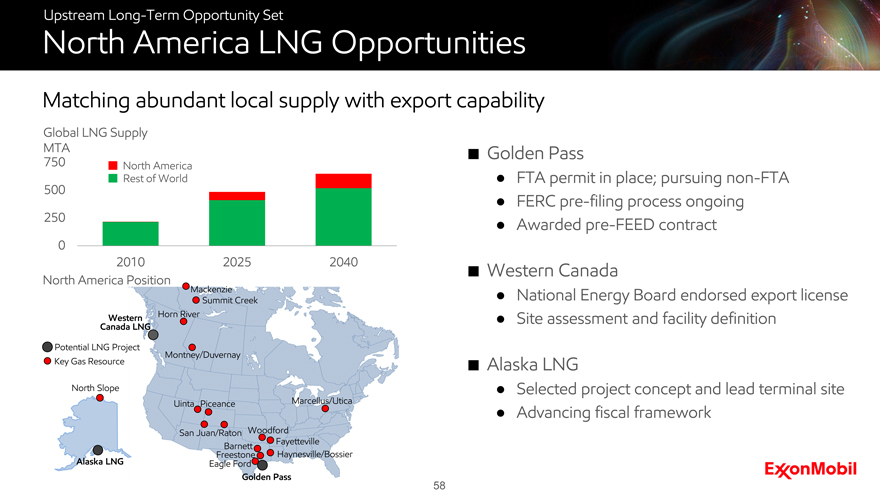

Upstream Long-Term Opportunity Set

North America LNG Opportunities

Matching abundant local supply with export capability

Global LNG Supply

MTA 750 500 250 0

2010 2025 2040

North America

Rest of world

North America Position

Golden Pass

FTA permit in place; pursuing non-FTA

FERC pre-filing process ongoing

Awarded pre-FEED contract

Western Canada

National Energy Board endorsed export license

Site assessment and facility definition

Alaska LNG

Selected project concept and lead terminal site

Advancing fiscal framework

58

Upstream Long-Term Opportunity Set

Upstream Summary

Well positioned for long-term profitable growth

Superior resource base

Large new opportunity set

Project selectivity and capital efficiency

Unlock potential through capabilities

Leading project development expertise

59

Strengthening the Downstream & Chemical Portfolio

Mike Dolan

Senior Vice President

Strengthening the Downstream and Chemical Portfolio

Premier Businesses

Sustained industry-leading results

Best-in-class operations

Flexibility and optimization tools

Technology-enabled, high-value product growth

Industry-leading portfolio

Pacesetter integrated facilities

Disciplined portfolio management

Robust pipeline of investments

Superior financial performance

Best-in-class returns

Strong cash generation

61

Strengthening the Downstream and Chemical Portfolio

Increasing Advantage in the Downstream

Focus on strategic assets

Lowering raw material cost

Increasing high-value product yield

Expanding logistics capability

Reducing operating cost

Disciplined portfolio management

62

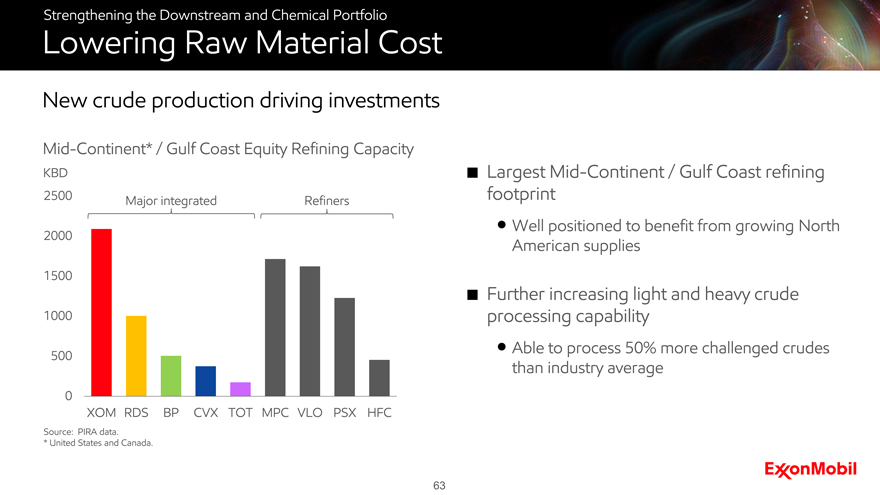

Strengthening the Downstream and Chemical Portfolio

Lowering Raw Material Cost

New crude production driving investments

Mid-Continent* / Gulf Coast Equity Refining Capacity

KBD

Source: PIRA data.

| * |

|

United States and Canada. |

Largest Mid-Continent / Gulf Coast refining footprint

Well positioned to benefit from growing North American supplies

Further increasing light and heavy crude processing capability

Able to process 50% more challenged crudes than industry average

2500 2000 1500 1000 500 0 XOM RDS BP CVX TOT MPC VLO PSX HFC

Major Integrated Refiners

63

Strengthening the Downstream and Chemical Portfolio

Increasing High Value Product Yield

Expanding diesel and lubes production

Increased diesel capacity in Singapore and Saudi Arabia

Developing coker project at Antwerp

Expanding high-performance lube basestock capacity

Blend plant investments support finished lubricant sales growth

64

Strengthening the Downstream and Chemical Portfolio

Strategic Investments in Chemical

Developing major projects in United States, Saudi Arabia, and Singapore

Capture advantaged feedstocks

Reduce production costs

Increase high-value products

Leverage integration

Target growth markets

65

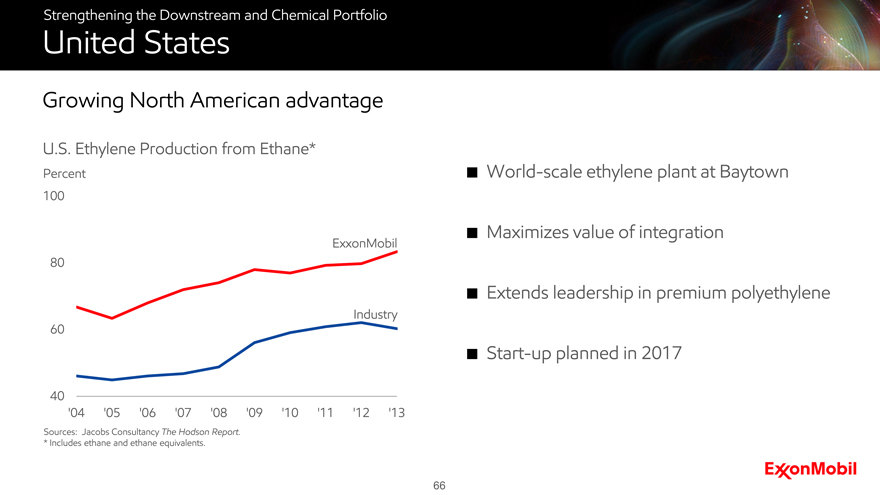

Strengthening the Downstream and Chemical Portfolio

United States

Growing North American advantage

U.S. Ethylene Production from Ethane*

Percent

Sources: Jacobs Consultancy The Hodson Report. * Includes ethane and ethane equivalents.

World-scale ethylene plant at Baytown

Maximizes value of integration

Extends leadership in premium polyethylene

Start-up planned in 2017

Percent 100 80 60 40 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13

ExxonMobil Industry

66

Strengthening the Downstream and Chemical Portfolio

Saudi Arabia

Expanding specialties footprint

World-scale synthetic rubber and elastomer facilities

Builds on existing JV platform

Supports development of rubber value chain

On plan for 2015 start-up

67

Strengthening the Downstream and Chemical Portfolio

Singapore

Serving Asia Pacific growth markets

Adding synthetic rubber and adhesive products

World-scale, based on advantaged feedstocks

Lower-cost production via integration

Start-up planned for 2017

68

Strengthening the Downstream and Chemical Portfolio

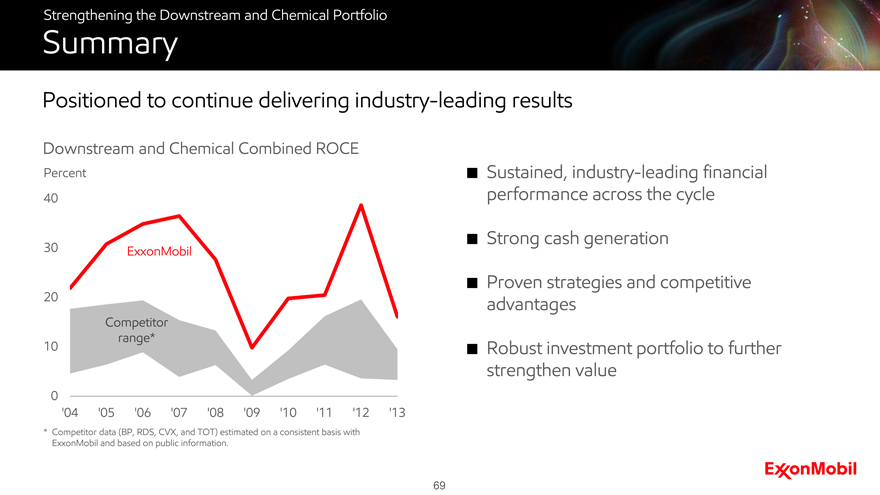

Summary

Positioned to continue delivering industry-leading results

Downstream and Chemical Combined ROCE

Percent

40 30 20 10 0

Exxon Mobil

Competitor range*

‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13

Sustained, industry-leading financial performance across the cycle

Strong cash generation

Proven strategies and competitive advantages

Robust investment portfolio to further strengthen value

* Competitor data (BP, RDS, CVX, and TOT) estimated on a consistent basis with ExxonMobil and based on public information.

69

Break

Summary

Rex Tillerson

Chairman and CEO

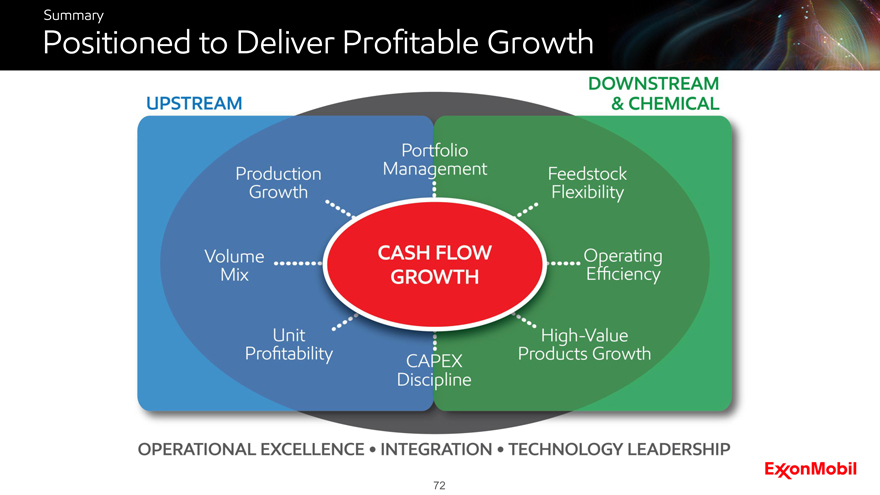

Summary

Positioned to Deliver Profitable Growth

72

Summary

Key Messages

Maintaining relentless focus on risk management and operational excellence

Major project start-ups delivering production volume growth through 2017

Improving Upstream unit profitability

Developing a unique and balanced set of profitable growth opportunities

Continuing disciplined capital allocation

Growing free cash flow and generating long-term shareholder value

73

Q&A