UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a)

of the Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ Preliminary Proxy Statement | ¨ Confidential, for Use of the Commission Only(as permitted by Rule 14a-6(e)(2)) | |

|

x Definitive Proxy Statement |

||

| ¨ Definitive Additional Materials | ||

| ¨ Soliciting Material Pursuant to §240.14a-12 | ||

EXXON MOBIL CORPORATION

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

| NOTICE OF 2008 | ||||

| ANNUAL MEETING | ||||

| AND PROXY STATEMENT |

| |||

| April 10, 2008 | ||||

Dear Shareholder:

We invite you to attend the annual meeting of shareholders on Wednesday, May 28, 2008, at the Morton H. Meyerson Symphony Center, 2301 Flora Street, Dallas, Texas 75201. The meeting will begin promptly at 9:00 a.m., Central Time. At the meeting, you will hear a report on our business and vote on the following items:

| Ÿ | Election of directors; |

| Ÿ | Ratification of independent auditors; |

| Ÿ | Seventeen shareholder proposals; and, |

| Ÿ | Other matters if properly raised. |

Only shareholders of record on April 4, 2008, or their proxy holders may vote at the meeting. Attendance at the meeting is limited to shareholders or their proxy holders and ExxonMobil’s guests. Only shareholders or their valid proxy holders may address the meeting.

This booklet includes the formal notice of the meeting, proxy statement, and financial statements. The proxy statement tells you about the agenda, procedures, and rules of conduct for the meeting. It also describes how the Board operates, gives information about our director candidates, and provides information about the other items of business to be conducted at the meeting.

Even if you own only a few shares, we want your shares to be represented at the meeting. You can vote your shares by Internet, toll-free telephone call, or proxy card.

To attend the meeting in person, please follow the instructions on page 3. A live audiocast of the meeting and a report on the meeting will be available on our Web site at exxonmobil.com.

Sincerely,

|

| |||

| Henry H. Hubble | Rex W. Tillerson | |||

| Secretary | Chairman of the Board |

| Page | ||

| 1 | ||

| 4 | ||

| 4 | ||

| 12 | ||

| 15 | ||

| 18 | ||

| 19 | ||

| 19 | ||

| 33 | ||

| 46 | ||

| 47 | ||

| 49 | ||

| 49 | ||

| 49 | ||

| 50 | ||

| 52 | ||

| Item 7 – Shareholder Advisory Vote on Executive Compensation |

53 | |

| 55 | ||

| 57 | ||

| 58 | ||

| 60 | ||

| 61 | ||

| 63 | ||

| 65 | ||

| 66 | ||

| 68 | ||

| 69 | ||

| 70 | ||

| 71 | ||

| 73 | ||

| A1 | ||

| A65 | ||

Who May Vote

Shareholders of ExxonMobil, as recorded in our stock register on April 4, 2008, may vote at the meeting.

How to Vote

You may vote in person at the meeting or by proxy. We recommend you vote by proxy even if you plan to attend the meeting. You can always change your vote at the meeting.

Important Notice Regarding the Availability of Proxy Materials for the Shareholder Meeting to be Held on May 28, 2008.

| Ÿ | The 2008 Proxy Statement and 2007 Summary Annual Report are available at www.edocumentview.com/xom |

Electronic Delivery of Proxy Statement and Annual Report

Instead of receiving future copies of these documents by mail, shareholders can elect to receive an e-mail that will provide electronic links to them. Opting to receive your proxy materials online will save the Company the cost of producing and mailing documents to your home or business, and also will give you an electronic link to the proxy voting site.

| Ÿ | Shareholders of Record: If you vote on the Internet at www.investorvote.com/exxonmobil, simply follow the prompts for enrolling in the electronic proxy delivery service. You also may enroll in the electronic proxy delivery service at any time in the future by going directly to computershare.com/exxonmobil. You may also revoke an electronic delivery election at this site at any time. |

| Ÿ | Beneficial Shareholders: If you hold your shares in a brokerage account, you also may have the opportunity to receive copies of the proxy materials electronically. Please check the information provided in the proxy materials mailed to you by your bank or broker regarding the availability of this service. |

How Proxies Work

ExxonMobil’s Board of Directors is asking for your proxy. Giving us your proxy means you authorize us to vote your shares at the meeting in the manner you direct. You may vote for all, some, or none of our director candidates. You may also vote for or against the other proposals, or abstain from voting.

If your shares are held in your name, you can vote by proxy in one of three convenient ways:

| Ÿ | Via Internet: Go to www.investorvote.com/exxonmobil and follow the instructions. You will need to have your proxy card in hand. At this Web site, you can elect to access future proxy statements and annual reports via the Internet. |

| Ÿ | By Telephone: Call toll-free 1-800-652-8683 (within the United States, Canada, and Puerto Rico) or 1-781-575-2300 (outside the United States, Canada, and Puerto Rico), and follow the instructions. You will need to have your proxy card in hand. |

| Ÿ | In Writing: Complete, sign, date, and return your proxy card in the enclosed envelope. |

Your proxy card covers all shares registered in your name and shares held in your Computershare Investment Plan account. If you own shares in the ExxonMobil Savings Plan for employees and retirees, your proxy card also covers those shares.

1

If you give us your signed proxy but do not specify how to vote, we will vote your shares in favor of our director candidates; in favor of the ratification of the appointment of independent auditors; and against the shareholder proposals.

If you hold shares through someone else, such as a stockbroker, you will receive material from that firm asking how you want to vote. Check the voting form used by that firm to see if it offers Internet or telephone voting.

Voting Shares in the ExxonMobil Savings Plan

The trustee of the ExxonMobil Savings Plan will vote Plan shares as participants direct. To the extent participants do not give instructions, the trustee will vote shares as it thinks best. The proxy card serves to give voting instructions to the trustee.

Revoking a Proxy

You may revoke your proxy before it is voted at the meeting by:

| Ÿ | Submitting a new proxy with a later date via a proxy card, the Internet, or by telephone; |

| Ÿ | Notifying ExxonMobil’s Secretary in writing before the meeting; or, |

| Ÿ | Voting in person at the meeting. |

Confidential Voting

Independent inspectors count the votes. Your individual vote is kept confidential from us unless special circumstances exist. For example, a copy of your proxy card will be sent to us if you write comments on the card.

Quorum

In order to carry on the business of the meeting, we must have a quorum. This means at least a majority of the outstanding shares eligible to vote must be represented at the meeting, either by proxy or in person. Treasury shares, which are shares owned by ExxonMobil itself, are not voted and do not count for this purpose.

Votes Required

| Ÿ | Election of Directors Proposal: A plurality of the votes cast is required for the election of directors. This means that the director nominee with the most votes for a particular seat is elected for that seat. Only votes FOR or WITHHELD count. Abstentions are not counted for purposes of the election of directors. |

Our Corporate Governance Guidelines, which can be found in the Corporate Governance section of our Web site at exxonmobil.com/governance, state that all directors will stand for election at the annual meeting of shareholders. In any non-contested election of directors, any director nominee who receives a greater number of votes WITHHELD from his or her election than votes FOR such election shall tender his or her resignation. Within 90 days after certification of the election results, the Board of Directors will decide, through a process managed by the Board Affairs Committee and excluding the nominee in question, whether to accept the resignation. Absent a compelling reason for the director to remain on the Board, the Board shall accept the resignation. The Board will promptly disclose its decision and, if applicable, the reasons for rejecting the tendered resignation on Form 8-K filed with the Securities and Exchange Commission (SEC).

| Ÿ | Other Proposals: Approval of the Ratification of Independent Auditors proposal and the shareholder proposals requires the favorable vote of a majority of the votes cast. Only votes FOR or AGAINST these proposals count. Abstentions and broker non-votes count for quorum purposes, but not for the voting of these proposals. A “broker non-vote” occurs when a bank, broker, or other |

2

| holder of record holding shares for a beneficial owner does not vote on a particular proposal because that holder does not have discretionary voting power for that particular item and has not received instructions from the beneficial owner. |

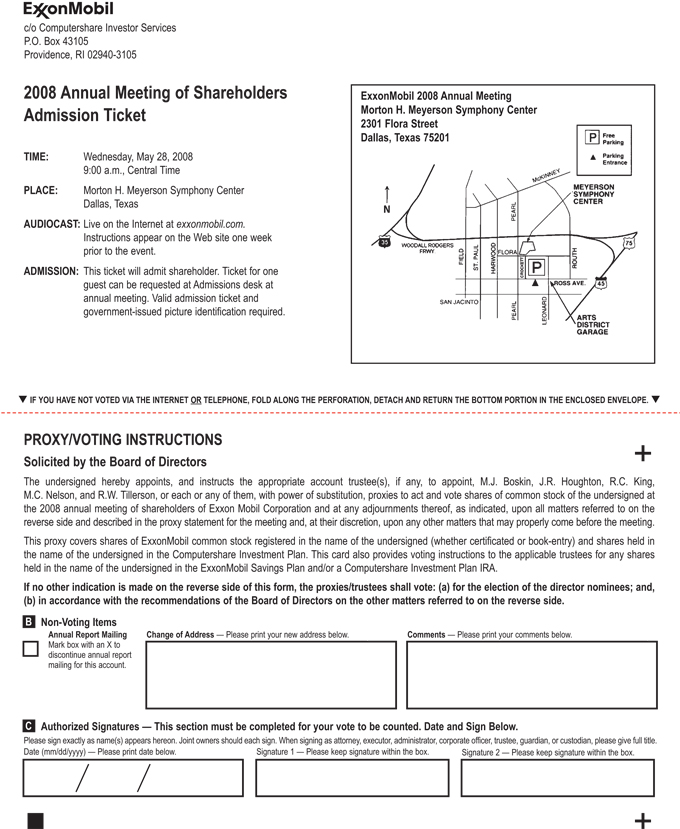

Annual Meeting Admission

Only shareholders or their proxy holders and ExxonMobil’s guests may attend the meeting. For safety and security reasons, no cameras, camera phones, recording equipment, electronic devices, large bags, briefcases, or packages will be permitted in the meeting. In addition, each shareholder and ExxonMobil’s guest will be asked to present a valid government-issued picture identification, such as a driver’s license, before being admitted to the meeting.

For registered shareholders, an admission ticket is attached to your proxy card. Please detach and bring the admission ticket with you to the meeting.

If your shares are held in the name of your broker, bank, or other nominee, you must bring to the meeting an account statement or letter from the nominee indicating that you beneficially owned the shares on April 4, 2008, the record date for voting. You may receive an admission ticket in advance by sending a written request with proof of ownership to the address listed under “Contact Information” below.

Shareholders who do not present admission tickets at the meeting will be admitted only upon verification of ownership at the admission counter.

Audiocast of the Annual Meeting

You are invited to visit our Web site at exxonmobil.com to hear the live audiocast of the meeting at 9:00 a.m., Central Time, on Wednesday, May 28, 2008. An archived copy of this audiocast will be available on our Web site for one year.

Conduct of the Meeting

The Chairman has broad responsibility and legal authority to conduct the annual meeting in an orderly and timely manner. This authority includes establishing rules for shareholders who wish to address the meeting. Only shareholders or their valid proxy holders may address the meeting. Copies of these rules will be available at the meeting. The Chairman may also exercise broad discretion in recognizing shareholders who wish to speak and in determining the extent of discussion on each item of business. In light of the number of business items on this year’s agenda and the need to conclude the meeting within a reasonable period of time, we cannot assure that every shareholder who wishes to speak on an item of business will be able to do so.

Dialogue can better be accomplished with interested parties outside the meeting and, for this purpose, we have provided a method for raising issues and contacting the non-employee directors either in writing or electronically on our Web site at exxonmobil.com/directors. The Chairman may also rely on applicable law regarding disruptions or disorderly conduct to ensure that the meeting is conducted in a manner that is fair to all shareholders. Shareholders making comments during the meeting must do so in English so that the majority of shareholders present can understand what is being said.

Contact Information

If you have questions or need more information about the annual meeting, write to:

Mr. Henry H. Hubble

Secretary

Exxon Mobil Corporation

5959 Las Colinas Boulevard

Irving, TX 75039-2298

call us at 1-972-444-1157,

or send a fax to us at 1-972-444-1505.

3

For information about shares registered in your name or your Computershare Investment Plan account, call ExxonMobil Shareholder Services at 1-800-252-1800 (within the United States, Canada, and Puerto Rico), or 1-781-575-2058 (outside the United States, Canada, and Puerto Rico), or access your account via the Web site at computershare.com/exxonmobil. We also invite you to visit ExxonMobil’s Web site at exxonmobil.com. Investor information can be found at exxonmobil.com/investor. Web site materials are not part of this proxy solicitation.

Overview

The Board of Directors and its committees perform a number of functions for ExxonMobil and its shareholders, including:

| Ÿ | Overseeing the management of the Company on your behalf; |

| Ÿ | Reviewing ExxonMobil’s long-term strategic plans; |

| Ÿ | Exercising direct decision-making authority in key areas, such as declaring dividends; |

| Ÿ | Selecting the CEO and evaluating the CEO’s performance; and, |

| Ÿ | Reviewing development and succession plans for ExxonMobil’s top executives. |

The Board has adopted Corporate Governance Guidelines that govern the structure and functioning of the Board and set out the Board’s position on a number of governance issues. A copy of our current Corporate Governance Guidelines is posted on our Web site at exxonmobil.com/governance. The Guidelines are also available to any shareholder on request to the Secretary at the address given under “Contact Information” on page 3.

All ExxonMobil directors stand for election at the annual meeting. Non-employee directors cannot stand for election after they have reached age 72, unless the Board makes an exception on a case-by-case basis. Employee directors resign from the Board when they are no longer employed by ExxonMobil.

Director Independence

Our Corporate Governance Guidelines require that a substantial majority of the Board consist of independent directors. In general, the Guidelines require that an independent director must have no material relationship with ExxonMobil, directly or indirectly, except as a director. The Board determines independence on the basis of the standards specified by the New York Stock Exchange (NYSE); the additional categorical standards referenced in our Corporate Governance Guidelines; and other facts and circumstances the Board considers relevant.

The NYSE standards generally provide that a director will not be independent if: (1) the director is, or in the past three years has been, an employee of ExxonMobil; or a member of the director’s immediate family is, or in the past three years has been, an executive officer of ExxonMobil; (2) the director or a member of the director’s immediate family has received more than $100,000 per year in direct compensation from ExxonMobil other than for service as a director; (3) the director or a member of the director’s immediate family currently is a partner of PricewaterhouseCoopers LLP (PwC), our independent auditors; or an employee in PwC’s audit, assurance, or tax compliance practices; or within the past three years has been a PwC partner or employee who worked on ExxonMobil’s audit; (4) the director or a member of the director’s immediate family is, or in the past three years has been, employed as an executive officer of a company where an ExxonMobil executive officer serves on the compensation committee; or, (5) the director or a member of the director’s immediate family is an executive officer of a

4

company that makes payments to, or receives payments from, ExxonMobil in an amount which, in any 12-month period during the past three years, exceeds the greater of $1 million or 2 percent of that other company’s consolidated gross revenues.

ExxonMobil’s Corporate Governance Guidelines also provide that a director will not be independent if a reportable “related person transaction” exists with respect to that director or a member of the director’s family for the current or most recently completed fiscal year. See the Guidelines for Review of Related Person Transactions posted on the Corporate Governance section of our Web site and described in more detail under “Related Person Transactions and Procedures” below. The categorical standards provided in the Related Person Transaction Guidelines also serve as ExxonMobil’s additional categorical standards for determining director independence.

The Board has reviewed relevant relationships between ExxonMobil and each non-employee director to determine compliance with the NYSE standards and ExxonMobil’s additional categorical standards. The Board has also evaluated whether there are any other facts or circumstances that might impair a director’s independence. Based on that review, the Board has determined that all ExxonMobil non-employee directors and director nominees (M.J. Boskin, L.R. Faulkner, W.W. George, J.R. Houghton, W.R. Howell, R.C. King, P.E. Lippincott, M.C. Nelson, S.J. Palmisano, S.S Reinemund, W.V. Shipley, and E.E. Whitacre, Jr.) are independent. The Board has also determined that each member of the Audit, Board Affairs, and Compensation Committees (see membership table below) is independent.

In recommending that each director and nominee be found independent, the Board Affairs Committee reviewed the following transactions, relationships, or arrangements. All matters described below fall within the NYSE and ExxonMobil independence standards.

| Name | Matters Considered | |

| M.C. Nelson |

Ordinary course business with Carlson (purchases of travel services; sales of lubricants) | |

| S.J. Palmisano |

Ordinary course business with IBM (purchases of consulting and IT maintenance services; sales of fuel and oil) |

Board Meetings and Committees; Annual Meeting Attendance

The Board met 10 times in 2007. ExxonMobil’s incumbent directors, on average, attended approximately 97 percent of Board and committee meetings during 2007; and no director attended less than 75 percent of such meetings.

As specified in our Corporate Governance Guidelines, it is ExxonMobil’s policy that directors should make every effort to attend the annual meeting of shareholders. All incumbent directors attended last year’s meeting except for Dr. Faulkner, who was first elected to the Board in January 2008.

ExxonMobil’s non-employee directors held five executive sessions of the independent directors in 2007. Normally, the Chair of the Board Affairs Committee (Mr. Shipley) or the Chair of the Compensation Committee (Mr. Howell) presides at executive sessions on a rotational basis, but the non-employee directors may, in light of the subject matter under discussion, select another Presiding Director for a particular session.

The Board appoints committees to help carry out its duties. Board committees work on key issues in greater detail than would be possible at full Board meetings. Only non-employee directors may serve on the Audit, Compensation, Board Affairs, Contributions, and Public Issues Committees. Each Committee has a written charter. The charters are posted on the Corporate Governance section of our Web site and are available free of charge on request to the Secretary at the address given under “Contact Information” on page 3.

5

The table below shows the current membership of each Board committee and the number of meetings each Committee held in 2007.

| Director | Audit | Compensation | Board Affairs |

Contributions | Finance | Public Issues |

Executive(1) | |||||||

| M.J. Boskin |

Ÿ | Ÿ | ||||||||||||

| L.R. Faulkner |

Ÿ | Ÿ | ||||||||||||

| W.W. George |

Ÿ | Ÿ | Ÿ | |||||||||||

| J.R. Houghton |

C | Ÿ | Ÿ | |||||||||||

| W.R. Howell |

C | Ÿ | Ÿ | |||||||||||

| R.C. King |

Ÿ | Ÿ | C | |||||||||||

| P.E. Lippincott |

Ÿ | Ÿ | Ÿ | |||||||||||

| M.C. Nelson |

Ÿ | C | Ÿ | Ÿ | ||||||||||

| S.J. Palmisano |

Ÿ | Ÿ | Ÿ | |||||||||||

| S.S Reinemund |

Ÿ | Ÿ | ||||||||||||

| W.V. Shipley |

C | Ÿ | ||||||||||||

| R.W. Tillerson |

C | C | ||||||||||||

| 2007 Meetings |

11 | 8 | 6 | 3 | 2 | 4 | 1 |

| C | = Chair |

| Ÿ | = Member |

| (1) | Other directors serve as alternate members on a rotational basis. |

Below is additional information about each Board committee.

Board Affairs Committee

The Board Affairs Committee serves as ExxonMobil’s nominating and corporate governance committee. The Committee recommends director candidates, reviews non-employee director compensation, and reviews other corporate governance practices, including the Corporate Governance Guidelines. The Committee also reviews any issue involving an executive officer or director under ExxonMobil’s Code of Ethics and Business Conduct and administers ExxonMobil’s Related Person Transaction Guidelines.

The Committee has adopted Guidelines for the Selection of Non-Employee Directors that describe the qualifications the Committee looks for in director candidates. These Selection Guidelines, as well as the Committee’s charter, are posted on the Corporate Governance section of our Web site.

The Selection Guidelines provide that candidates for non-employee director of ExxonMobil should be individuals who have achieved prominence in their fields, with experience and demonstrated expertise in managing large, relatively complex organizations, and/or, in a professional or scientific capacity, be accustomed to dealing with complex situations preferably with worldwide scope.

A substantial majority of the Board must meet the independence standards described in the Corporation’s Corporate Governance Guidelines, and all candidates must be free from any relationship with management or the Corporation that would interfere with the exercise of independent judgment. Candidates should be committed to representing the interests of all shareholders and not any particular constituency.

The Board believes a director should be able to serve for several years. Candidates should bring integrity, insight, energy, and analytical skills to Board deliberations, and must have a commitment to devote the necessary time and attention to oversee the affairs of a corporation as large and complex as ExxonMobil. ExxonMobil recognizes that the strength and effectiveness of the Board reflect the balance,

6

experience, and diversity of the individual directors; their commitment; and importantly, the ability of directors to work effectively as a group in carrying out their responsibilities. ExxonMobil seeks candidates with diverse backgrounds who possess knowledge and skills in areas of importance to the Corporation. The Board must include members with particular experience required for service on key Board committees, as described in the committee charters on our Web site.

The Committee identifies director candidates primarily through recommendations made by the non-employee directors. These recommendations are developed based on the directors’ own knowledge and experience in a variety of fields, and research conducted by ExxonMobil staff at the Committee’s direction. The Committee also considers recommendations made by the employee directors, shareholders, and others, including search firms. The Committee has the authority to engage consultants to help identify or evaluate potential director nominees. All recommendations, regardless of the source, are evaluated on the same basis against the criteria contained in the Selection Guidelines.

Dr. Faulkner was initially suggested as a candidate by the Chief Executive Officer and subsequently recommended for nomination by the incumbent non-employee directors on the Board Affairs Committee. The recommendation of Mr. Whitacre was made by the incumbent non-employee directors on the Board Affairs Committee.

Shareholders may send recommendations for director candidates to the Secretary at the address given under “Contact Information” on page 3. A submission recommending a candidate should include:

| Ÿ | Sufficient biographical information to allow the Committee to evaluate the candidate in light of the Selection Guidelines; |

| Ÿ | Information concerning any relationship between the candidate and the shareholder recommending the candidate; and, |

| Ÿ | Material indicating the willingness of the candidate to serve if nominated and elected. |

The procedures by which shareholders may recommend nominees have not changed materially since last year’s proxy statement.

The Committee is also responsible for reviewing and making recommendations to the Board regarding the compensation of the non-employee directors. The Committee uses an independent consultant, Pearl Meyer & Partners, to provide information on current developments and practices in director compensation. Pearl Meyer & Partners is the same consultant retained by the Compensation Committee to advise on executive compensation, but performs no other work for ExxonMobil.

Audit Committee

The Audit Committee oversees accounting and internal control matters. Its responsibilities include oversight of:

| Ÿ | Management’s conduct of the Corporation’s financial reporting process; |

| Ÿ | The integrity of the financial statements and other financial information provided by the Corporation to the SEC and the public; |

| Ÿ | The Corporation’s system of internal accounting and financial controls; |

| Ÿ | The Corporation’s compliance with legal and regulatory requirements; |

| Ÿ | The performance of the Corporation’s internal audit function; |

| Ÿ | The independent auditors’ qualifications, performance, and independence; and, |

| Ÿ | The annual independent audit of the Corporation’s financial statements. |

The Committee has direct authority and responsibility to appoint (subject to shareholder ratification), compensate, retain, and oversee the independent auditors.

7

The Committee also prepares the report that the SEC rules require be included in the Corporation’s annual proxy statement. This report is on pages 46-47.

The Committee has adopted specific policies and procedures for pre-approving fees paid to the independent auditors. These policies and procedures, as well as the Committee’s charter, are posted on the Corporate Governance section of our Web site.

The Board has determined that all members of the Committee are financially literate within the meaning of the NYSE standards, and that Dr. Faulkner, Mr. Houghton, Mr. Lippincott, and Mr. Reinemund are “audit committee financial experts” as defined in the SEC rules.

Compensation Committee

The Compensation Committee oversees compensation for ExxonMobil’s senior executives, including their salary, bonus, and incentive awards, and succession plans for key executive positions. The Committee’s charter is available on the Corporate Governance section of our Web site.

During 2007, the Committee established the ceiling for the 2007 short term and long term incentive award programs; endorsed the salary program for 2008; reviewed the individual performance and contributions of each senior executive; granted individual incentive awards and set salaries for the senior executives; and, reviewed progress on executive development and succession planning for senior positions. In addition, the Committee endorsed several program changes as described on page 32.

The Compensation Committee’s report is on page 19.

The Committee does not delegate its responsibilities with respect to ExxonMobil’s executive officers and other senior executives (approximately 24 positions). For other employees, the Committee delegates authority to determine individual salaries and incentive awards to a committee consisting of the Chairman and the Senior Vice Presidents of the Corporation. That committee’s actions are subject to a salary budget and aggregate annual ceilings on cash and equity incentive awards established by the Compensation Committee.

The Committee utilizes the expertise of an external independent consultant, Pearl Meyer & Partners, whom the Committee retains and works with during the year. At the direction of the Chair of the Compensation Committee, the consultant provides the following services:

| Ÿ | Attends meetings of the Compensation Committee. |

| Ÿ | Makes an annual presentation to the Compensation Committee regarding: |

| – | General trends in executive compensation across industries, particularly trends that reflect a change in compensation practices. The consultant advises the Committee on whether changes in compensation practices are relevant to ExxonMobil’s compensation programs. |

| – | A perspective on the structure and competitive standing of ExxonMobil’s compensation program for senior executives. |

| Ÿ | Participates in the Committee’s deliberations regarding compensation for Named Executive Officers that include items such as: |

| – | How to interpret the level of compensation of each Named Executive Officer compared to similar positions across industries. |

| – | The appropriate level of each element of compensation for individual Named Executive Officers considering their career experience and tenure in their positions, as well as general performance of the Company within the industry. |

| – | The pace at which compensation levels should be adjusted over future years. |

| – | How to weigh or consider the impact of a compensation change today on future retirement income. |

8

| – | The interpretation of issues involving executive compensation raised by shareholders and the appropriate responses from management. |

| – | The relationship between compensation and executive succession planning. |

| – | How the Committee should emphasize or weigh one element of compensation versus another to address the long-term nature of the business and long planning lead times. |

| Ÿ | Prepares the analysis of comparator company compensation used by the Compensation Committee. |

The input of the independent consultant is given serious consideration as part of the Committee’s decision-making process but is not assigned a weight versus the other matters considered by the Committee as described in the “Compensation Discussion and Analysis” beginning on page 19.

In addition, at the direction of the Chair of the Board Affairs Committee, Pearl Meyer & Partners provides an annual survey of non-employee director compensation for use by that Committee.

ExxonMobil management does not use Pearl Meyer & Partners to advise on ExxonMobil’s general employee compensation and benefit programs. The Chair of the Compensation Committee negotiates the terms of Pearl Meyer & Partners’ engagement.

The Committee meets with ExxonMobil’s Chairman and other senior executives during the year to review the Corporation’s business results and progress against strategic plans. The Committee uses this input to help determine the aggregate annual ceilings to be set for the Corporation’s cash and equity incentive award programs. The Chairman also provides input to the Committee regarding performance assessments for ExxonMobil’s other senior executives and makes recommendations to the Committee with respect to salary and incentive awards for these executives and succession planning for senior positions.

The Committee uses tally sheets to assess total compensation for the Corporation’s senior executives under different scenarios. The tally sheets value all elements of cash compensation; incentive awards, including restricted stock grants; the annual change in pension value; and other benefits and perquisites. The tally sheets also display the value of outstanding awards and lump sum pension estimates. For tally sheet purposes, the Committee considers restricted stock awards on the basis of grant date fair value as shown in the “Grants of Plan-Based Awards” table, not on the financial accounting method used for the “Summary Compensation Table.”

See page 26 for additional information on tally sheets and the “Compensation Discussion and Analysis” beginning on page 19 for more information on the Committee’s approach to executive compensation and the decisions made by the Committee for 2007.

Advisory Committee on Contributions

The Advisory Committee on Contributions reviews the level of ExxonMobil’s support for education and other public service programs, including the Company’s contributions to the ExxonMobil Foundation. The Foundation works to improve the quality of education in the U.S. at all levels, with special emphasis on math and science. The Foundation also supports the Company’s other cultural and public service giving. The Committee’s charter is available on the Corporate Governance section of our Web site.

Finance Committee

The Finance Committee reviews ExxonMobil’s financial policies and strategies, including our capital structure, dividends, and share repurchase program. The Committee authorizes the issuance of corporate debt subject to limits set by the Board. The Committee’s charter is available on the Corporate Governance section of our Web site.

Public Issues Committee

The Public Issues Committee reviews the effectiveness of the Corporation’s policies, programs, and practices with respect to safety, health, the environment, and social issues. The Committee hears reports

9

from operating units on safety and environmental activities. The Committee also visits operating sites to observe and comment on current operating practices. The Committee’s charter is available on the Corporate Governance section of our Web site.

Executive Committee

The Executive Committee has broad power to act on behalf of the Board. In practice, the Committee meets only when it is impractical to call a meeting of the full Board.

Shareholder Communications

The Board Affairs Committee has approved and implemented procedures for shareholders and other interested persons to send communications to individual directors or the non-employee directors as a group.

| Ÿ | Written Communications: Written correspondence should be addressed to the director or directors in care of the Secretary at the address given under “Contact Information” on page 3. All correspondence either will be forwarded to the intended recipient and to the Chair of the Board Affairs Committee, as appropriate, or held for review before or after the next regular Board meeting. A log of all correspondence addressed to the directors will also be kept for periodic review by the Board Affairs Committee and any other interested director. |

| Ÿ | Electronic Communications: You may also send e-mail to individual non-employee directors or the non-employee directors as a group by using the form provided for that purpose on our Web site at exxonmobil.com/directors. These communications are sent directly to the specified director’s electronic mailbox. E-mail can be viewed by staff of the Office of the Secretary, but can only be deleted by the director to whom it is addressed. More information about our procedures for handling communications to non-employee directors is posted on the Corporate Governance section of our Web site. |

Code of Ethics and Business Conduct

The Board maintains policies and procedures (which we refer to in this proxy statement as the “Code”) that represent both the code of ethics for the principal executive officer, principal financial officer, and principal accounting officer under SEC rules, and the code of business conduct and ethics for directors, officers, and employees under NYSE listing standards. The Code applies to all directors, officers, and employees. The Code includes a Conflicts of Interest Policy under which directors, officers, and employees are expected to avoid any actual or apparent conflict between their own personal interests and the interests of the Corporation.

The Code is posted on the Corporate Governance section of our Web site and is available free of charge on request to the Secretary at the address given under “Contact Information” on page 3. The Code is also included as an exhibit to our Annual Report on Form 10-K. Any amendment of the Code will be posted promptly on our Web site.

The Corporation maintains procedures for administering and reviewing potential issues under the Code, including procedures that allow employees to make complaints without identifying themselves. The Corporation also conducts periodic mandatory business practice training sessions and requires each regular employee and non-employee director to make an annual compliance certification.

The Board Affairs Committee will initially review any suspected violation of the Code involving an executive officer or director and will report its findings to the Board. The Board does not envision that any waiver of the Code will be granted. Should such a waiver occur, it will be promptly disclosed on our Web site.

10

Related Person Transactions and Procedures

In accordance with SEC rules, ExxonMobil maintains Guidelines for Review of Related Person Transactions. These Guidelines are available on the Corporate Governance section of our Web site.

In accordance with the Related Person Transaction Guidelines, all executive officers, directors, and director nominees are required to identify, to the best of their knowledge after reasonable inquiry, business and financial affiliations involving themselves or their immediate family members that could reasonably be expected to give rise to a reportable related person transaction. Covered persons must also advise the Secretary of the Corporation promptly of any change in the information provided, and will be asked periodically to review and re-affirm their information.

For the above purposes, “immediate family member” includes a person’s spouse, parents, siblings, children, in-laws, and step-relatives.

Based on this information, we review the Company’s own records and make follow-up inquiries as may be necessary to identify potentially reportable transactions. A report summarizing such transactions and including a reasonable level of detail is then provided to the Board Affairs Committee. The Committee oversees the Related Person Transaction Guidelines generally and reviews specific items to assess materiality.

In assessing materiality for this purpose, information will be considered material if, in light of all the circumstances, there is a substantial likelihood a reasonable investor would consider the information important in deciding whether to buy or sell ExxonMobil stock or in deciding how to vote shares of ExxonMobil stock. A director will abstain from the decision on any transactions involving that director or his or her family members.

Under SEC rules, certain transactions are deemed not to involve a material interest (including transactions in which the amount involved in any 12-month period is less than $120,000 and transactions with entities where a related person’s interest is limited to service as a non-employee director). In addition, based on a consideration of ExxonMobil’s facts and circumstances, the Committee will presume that the following transactions do not involve a material interest for purposes of reporting under SEC rules:

| Ÿ | Transactions in the ordinary course of business with an entity for which a related person serves as an executive officer, provided (1) the affected director or executive officer did not participate in the decision on the part of ExxonMobil to enter into such transactions; and, (2) the amount involved in any related category of transactions in a 12-month period is less than 1 percent of the entity’s gross revenues. |

| Ÿ | Grants or membership payments in the ordinary course of business to nonprofit organizations, provided (1) the affected director or executive officer did not participate in the decision on the part of ExxonMobil to make such payments; and, (2) the amount of general-purpose grants in a 12-month period is less than 1 percent of the recipient’s gross revenues. |

| Ÿ | Payments under ExxonMobil plans and arrangements that are available generally to U.S. salaried employees (including contributions under ExxonMobil’s Educational and Cultural Matching Gift Programs and payments to providers under ExxonMobil health care plans). |

| Ÿ | Employment by ExxonMobil of a family member of an executive officer, provided the executive officer does not participate in decisions regarding the hiring, performance evaluation, or compensation of the family member. |

Transactions or relationships not covered by the above standards will be assessed by the Committee on the basis of the specific facts and circumstances.

ExxonMobil and its affiliates have about 81,000 employees around the world and employees related by birth or marriage may be found at all levels of the organization. Two current executive officers have family members who are also employed by the Corporation: J.S. Simon (Senior Vice President and Director) has a son-in-law who works for ExxonMobil Fuels Marketing Company, and H.H. Hubble (Vice President, Investor Relations and Secretary) has a son who works for ExxonMobil Development Company.

11

ExxonMobil employees do not receive preferential treatment by reason of being related to an executive officer, and executive officers do not participate in hiring, performance evaluation, or compensation decisions for family members. ExxonMobil’s employment guidelines state “Relatives of Company employees may be employed on a non-preferential basis. However, an employee should not be employed by or assigned to work under the direct supervision of a relative, or to report to a supervisor who in turn reports to a relative of the employee.” Accordingly, consistent with ExxonMobil’s Related Person Transaction Guidelines, we do not consider the relationships noted above to be material within the meaning of the related person transaction disclosure rules.

P.T. Mulva (Vice President and Controller) has a brother currently serving as Chairman and CEO of ConocoPhillips. As is the case with most other major companies in the oil and gas industry, ExxonMobil has a variety of business transactions with ConocoPhillips. These transactions include routine purchases and sales of crude oil, petroleum products, and pipeline transportation capacity. Affiliates of ExxonMobil and ConocoPhillips have joint ownership of a refinery in Germany and a number of pipelines, terminals, emergency response companies, and service companies, and also have undivided interests in a variety of exploration, development, and production projects. All of these transactions are entered into in the ordinary course of business without influence from P.T. Mulva. Neither P.T. Mulva nor, to our knowledge after reasonable inquiry, his brother has any interest in these transactions different from the general interest of other employees and shareholders. Accordingly, consistent with ExxonMobil’s Related Person Transaction Guidelines, we do not consider these transactions to be material within the meaning of the related person transaction disclosure rules.

S.R. LaSala (Vice President and General Tax Counsel) has a son who is a partner of a law firm that performs work for ExxonMobil. Mr. LaSala is not involved in decisions to retain the firm and therefore we do not consider the relationship to be material within the meaning of the related person transaction disclosure rules.

The Board Affairs Committee also reviewed ExxonMobil’s ordinary course business with companies for which non-employee directors serve as executive officers and determined that, in accordance with the categorical standards described above, none of those matters represent reportable related person transactions. See “Director Independence” on page 4.

We are not aware of any related person transaction required to be reported under applicable SEC rules since the beginning of the last fiscal year where our policies and procedures did not require review, or where such policies and procedures were not followed.

The Corporation’s Related Person Transaction Guidelines are intended to assist the Corporation in complying with its disclosure obligations under SEC rules. These procedures are in addition to, not in lieu of, the Corporation’s Code of Ethics and Business Conduct.

ITEM 1 – ELECTION OF DIRECTORS

The Board of Directors has nominated the director candidates named on the following pages. Personal information on each of our nominees is also provided. All of our nominees currently serve as ExxonMobil directors except Mr. Whitacre, who has been nominated by the Board for first election as a director at the annual meeting. Dr. Faulkner was elected by the Board in January 2008. Messrs. Howell, Lippincott, and Simon have reached retirement age and are not standing for re-election. Messrs. Houghton and Shipley have reached the usual retirement age but are standing for re-election on an exception basis at the request of the Board.

If a director nominee becomes unavailable before the election, your proxy authorizes the people named as proxies to vote for a replacement nominee if the Board names one.

12

The Board recommends you vote FOR each of the following candidates:

| Michael J. Boskin

Age 62 Director since 1996 |

Principal Occupation: T.M. Friedman Professor of Economics and Senior Fellow, Hoover Institution, Stanford University

Recent Business Experience: Dr. Boskin is also a Research Associate, National Bureau of Economic Research; and serves on the Commerce Department’s Advisory Committee on the National Income and Product Accounts. He is Chief Executive Officer and President of Boskin & Co., an economic consulting company.

Public Company Directorships: Oracle Corporation; Shinsei Bank; Vodafone Group | |

| Larry R. Faulkner

Age 63 Director since 2008 |

Principal Occupation: President, Houston Endowment; President Emeritus, the University of Texas at Austin

Recent Business Experience: Dr. Faulkner served as President of the University of Texas at Austin from 1998 to 2006. He also served on the chemistry faculties of the University of Texas, the University of Illinois, and Harvard University. At the University of Illinois, he also held a number of positions in academic administration including Provost and Vice Chancellor for Academic Affairs.

Public Company Directorships: Temple-Inland; Guaranty Financial Group | |

| William W. George

Age 65 Director since 2005 |

Principal Occupation: Professor of Management Practice, Harvard University

Recent Business Experience: Mr. George was elected Chairman of Medtronic in 1996, and retired in 2002; Chief Executive Officer in 1991; and President and Chief Operating Officer in 1989.

Public Company Directorships: Goldman Sachs; Novartis | |

| James R. Houghton

Age 72 Director since 1994 |

Principal Occupation: Chairman of the Board Emeritus, Corning Incorporated

Recent Business Experience: Mr. Houghton retired as Non-Executive Chairman in 2007. He resumed his role as Chairman and Chief Executive Officer of Corning Incorporated in 2002, relinquished the role of CEO in 2005, and retired as Executive Chairman in 2006. He also served as Non-Executive Chairman from 2001 to 2002 and Chairman Emeritus from 1996 to 2001. He was elected Chairman and Chief Executive Officer of Corning Incorporated in 1983, retired in 1996.

Public Company Directorships: Corning Incorporated; MetLife | |

13

| Reatha Clark King

Age 70 Director since 1997 |

Principal Occupation: Former Chairman, Board of Trustees, General Mills Foundation

Recent Business Experience: Dr. King was elected Chairman, Board of Trustees, General Mills Foundation in 2002, and retired in 2003; President and Executive Director, General Mills Foundation, and Vice President, General Mills, Inc. from 1988 to 2002. Prior to joining the General Mills Foundation, Dr. King held a variety of positions in chemical research, education, and academic administration.

Public Company Directorships: Lenox Group | |

| Marilyn Carlson Nelson

Age 68 Director since 1991 |

Principal Occupation: Chairman of the Board, Carlson

Recent Business Experience: Mrs. Nelson was elected Chairman and Chief Executive Officer of Carlson in 1998, and relinquished the role of CEO in 2008. She has held a number of other management positions at Carlson including President, Chief Operating Officer, Vice Chair and Senior Vice President.

Company Directorships: Carlson | |

| Samuel J. Palmisano

Age 56 Director since 2006 |

Principal Occupation: Chairman of the Board, President, and Chief Executive Officer, IBM

Recent Business Experience: Mr. Palmisano was elected Chairman, President, and Chief Executive Officer of IBM in 2003. Mr. Palmisano also served as President, Senior Vice President, and Group Executive for IBM’s Enterprise Systems Group, IBM Global Services, and IBM’s Personal Systems Group.

Public Company Directorships: IBM | |

| Steven S Reinemund

Age 60 Director since 2007 |

Principal Occupation: Retired Executive Chairman of the Board, PepsiCo

Recent Business Experience: Mr. Reinemund served as Executive Chairman of the Board of PepsiCo from 2006 to 2007; was elected Chief Executive Officer and Chairman of the Board in 2001; President and Chief Operating Officer in 1999; and Director in 1996. He was also elected President and CEO of Frito-Lay in 1992 and Pizza Hut in 1986.

Public Company Directorships: Johnson & Johnson; American Express; Marriott | |

14

| Walter V. Shipley

Age 72 Director since 1998 |

Principal Occupation: Retired Chairman of the Board, The Chase Manhattan Corporation and The Chase Manhattan Bank

Recent Business Experience: Mr. Shipley was elected Chairman and Chief Executive Officer of Chase Manhattan upon its merger with Chemical Bank in 1996, and retired in 1999. He was elected Chairman and Chief Executive Officer of Chemical Bank in 1983; President and Director in 1982; and Senior Executive Vice President in 1979.

Public Company Directorships: None | |

| Rex W. Tillerson

Age 56 Director since 2004 |

Principal Occupation: Chairman of the Board and Chief Executive Officer, Exxon Mobil Corporation

Recent Business Experience: Mr. Tillerson was elected Chairman and Chief Executive Officer of ExxonMobil in 2006; President and Director in 2004; and Senior Vice President in 2001. Mr. Tillerson has held a variety of management positions in domestic and foreign operations since joining the Exxon organization in 1975, including President, Exxon Yemen Inc. and Esso Exploration and Production Khorat Inc.; Vice President, Exxon Ventures (CIS) Inc.; President, Exxon Neftegas Limited; and Executive Vice President, ExxonMobil Development Company.

Public Company Directorships: None | |

| Edward E. Whitacre, Jr.

Age 66 Director nominee |

Principal Occupation: Retired Chairman of the Board and Chief Executive Officer, AT&T

Recent Business Experience: Mr. Whitacre was elected Chairman and Chief Executive Officer of AT&T upon its merger with SBC Communications in 2005, and retired in 2007. He was elected Chairman and Chief Executive Officer of SBC in 1990; and President and Chief Operating Officer in 1988.

Public Company Directorships: Burlington Northern Santa Fe; Anheuser-Busch | |

Director compensation elements are designed to:

| Ÿ | Ensure alignment with long-term shareholder interests; |

| Ÿ | Ensure the Company can attract and retain outstanding director candidates who meet the selection criteria outlined in the Guidelines for Selection of Non-Employee Directors, which can be found in the Corporate Governance section of our Web site; |

| Ÿ | Recognize the substantial time commitments necessary to oversee the affairs of the Corporation; and, |

| Ÿ | Support the independence of thought and action expected of directors. |

15

Non-employee director compensation levels are reviewed by the Board Affairs Committee each year, and resulting recommendations are presented to the full Board for approval. The Committee uses an independent consultant, Pearl Meyer & Partners, to provide information on current developments and practices in director compensation. Pearl Meyer & Partners is the same consultant retained by the Compensation Committee to advise on executive compensation, but performs no other work for ExxonMobil.

ExxonMobil employees receive no extra pay for serving as directors. Non-employee directors receive compensation consisting of cash and restricted stock.

In 2007, the base cash retainer for non-employee directors was $75,000 per year. Members of the Audit and Compensation Committees received a fee of $15,000 per year, and the Chairs of those Committees received an additional fee of $10,000 per year. For other Committees, non-employee directors received $8,000 per year for each Committee on which they served, and the Chairs received an additional fee of $7,000 per year.

Effective January 1, 2008, non-employee director cash compensation was restructured to pay a higher base fee of $100,000 per year and to eliminate per committee and committee chair fees except for the Chairs of the Audit and Compensation Committees ($10,000).

Through 2007, non-employee directors could defer all or part of their cash compensation either in ExxonMobil notional stock with dividend equivalents, or in a deferred account earning interest at the prime rate. As of year-end 2007, the ability to defer director fees has been terminated. Accrued deferred account balances are being returned to participants in one or two annual installments that commenced in January 2008.

No fees are paid to members of the Executive Committee. Non-employee directors are reimbursed for reasonable expenses incurred to attend board meetings or other functions relating to their responsibilities as a director of Exxon Mobil Corporation.

In addition to the fees described above, we pay a significant portion of director compensation in stock to strongly align director compensation with the long-term interests of shareholders. Through 2007, each incumbent non-employee director except for Dr. Faulkner, who was first elected to the Board in January 2008, received an annual award of 4,000 shares of restricted stock. Effective January 1, 2008, the annual restricted stock grant was reduced from 4,000 shares to 2,500 to maintain alignment with equity compensation paid by comparator companies. In addition, each new non-employee director receives a one-time grant of 8,000 shares of restricted stock upon first being elected to the Board. While on the Board, the non-employee director receives the same cash dividends on restricted shares as a holder of regular common stock, but the director is not allowed to sell the shares. The restricted shares may be forfeited if the director leaves the Board early, i.e., before retirement age of 72, as specified for non-employee directors.

Current and former non-employee directors of Exxon Mobil Corporation are eligible to participate in the ExxonMobil Foundation’s Educational and Cultural Matching Gift Programs under the same terms as the Corporation’s U.S. employees.

16

Director Compensation for 2007

| Name |

Fees Earned or Paid in Cash ($) |

Stock Awards ($)(a) |

Option Awards ($) |

Non-Equity Incentive Plan Compensation ($) |

Change in Earnings ($)(b) |

Other Compensation ($)(c) |

Total ($) | |||||||

| M.J. Boskin |

104,182 | 298,540 | 0 | 0 | 0 | 318 | 403,040 | |||||||

| W.W. George |

106,000 | 298,540 | 0 | 0 | 0 | 318 | 404,858 | |||||||

| J.R. Houghton |

111,297 | 298,540 | 0 | 0 | 0 | 318 | 410,155 | |||||||

| W.R. Howell |

114,181 | 298,540 | 0 | 0 | 24,198 | 318 | 437,237 | |||||||

| R.C. King |

112,999 | 298,540 | 0 | 0 | 4,830 | 318 | 416,687 | |||||||

| P.E. Lippincott |

101,297 | 298,540 | 0 | 0 | 0 | 318 | 400,155 | |||||||

| H.A. McKinnell |

40,798 | 298,540 | 0 | 0 | 3,909 | 318 | 343,565 | |||||||

| M.C. Nelson |

106,000 | 298,540 | 0 | 0 | 0 | 318 | 404,858 | |||||||

| S.J. Palmisano |

106,000 | 298,540 | 0 | 0 | 0 | 318 | 404,858 | |||||||

| S.S Reinemund |

57,615 | 387,357 | 0 | 0 | 0 | 318 | 445,290 | |||||||

| W.V. Shipley |

104,181 | 298,540 | 0 | 0 | 0 | 318 | 403,039 |

| (a) | In accordance with SEC rules, the valuation of stock awards in this table represents the compensation cost of awards recognized for financial statement purposes for 2007 under Statement of Financial Accounting Standards No. 123, as revised (123R). The Company recognizes compensation cost for restricted stock granted to the non-employee director over a 12-month period following the grant date. Dividends on stock awards are not shown in the table because those amounts are factored into the grant date fair value. |

| Each director (other than Mr. Reinemund, who joined the Board in May 2007) received an annual grant of 4,000 restricted shares at the beginning of 2007. The compensation cost recognized for these awards and shown in the table for 2007 is the same as the grant date fair value of these grants, which was $298,540. |

| Mr. Reinemund received a one-time grant of 8,000 restricted shares upon being first elected to the Board in May 2007. The compensation cost recognized for this award and shown in the table for 2007 was seven-twelfths of the grant date fair value of this grant recognized in 2007, which was $387,357. |

| At year-end 2007, the aggregate number of restricted shares held by each director was as follows: |

| Name | Restricted Shares (#) | |

| M.J. Boskin |

44,300 | |

| W.W. George |

16,000 | |

| J.R. Houghton |

45,900 | |

| W.R. Howell |

49,900 | |

| R.C. King |

43,100 | |

| P.E. Lippincott |

49,900 | |

| M.C. Nelson |

48,300 | |

| S.J. Palmisano |

12,000 | |

| S.S Reinemund |

8,000 | |

| W.V. Shipley |

41,900 |

| (b) | The amounts shown are earnings during 2007 on interest-bearing deferred fee accounts that were in excess of the federal long-term interest rate published pursuant to Section 1274(d) of the Internal Revenue Code. The federal rate averaged approximately 6 percent during the year. The interest rate under the directors’ deferred fee plan is the prime rate, which averaged approximately 8 percent during 2007. |

| (c) | The amount shown for each director is the prorated cost of travel accident insurance covering death, dismemberment, and loss of sight, speech, or hearing under a policy purchased by the Corporation with a maximum benefit of $500,000 per individual. |

17

The non-employee directors are not entitled to any additional payments or benefits as a result of leaving the Board or death except as described above. The non-employee directors are not entitled to any payments or benefits resulting from a change in control of the Corporation.

DIRECTOR AND EXECUTIVE OFFICER STOCK OWNERSHIP

These tables show the number of ExxonMobil common stock shares each executive named in the “Summary Compensation Table” on page 33 and each non-employee director or director nominee owned on February 29, 2008 (or at retirement, if earlier). In these tables, ownership means the right to direct the voting or the sale of shares, even if those rights are shared with someone else. None of these individuals owns more than 0.02 percent of the outstanding shares.

| Named Executive Officer | Shares Owned | Shares Covered by Exercisable Options | |||

| R.W. Tillerson |

929,149 | (1) | 327,307 | ||

| D.D. Humphreys |

433,346 | (2) | 195,097 | ||

| S.R. McGill |

909,833 | (3) | 345,097 | ||

| J.S. Simon |

826,283 | (4) | 470,000 | ||

| H.R. Cramer |

607,492 | 529,964 | |||

| M.E. Foster |

496,169 | (5) | 215,097 | ||

| P.E. Sullivan |

432,973 | (6) | 309,943 |

| (1) | Includes 1,725 shares owned by dependent child. |

| (2) | Includes 58,927 shares jointly owned with spouse. |

| (3) | Includes 3,200 shares owned by spouse. |

| (4) | Includes 11,177 shares jointly owned with spouse. |

| (5) | Includes 676 shares owned by spouse and 13,789 shares owned by dependent children. |

| (6) | Includes 94,696 shares jointly owned with spouse. |

| Non-Employee Director/Nominee | Shares Owned | ||

| M.J. Boskin |

46,800 | ||

| L.R. Faulkner |

8,000 | ||

| W.W. George |

58,500 | (1) | |

| J.R. Houghton |

55,400 | (2) | |

| W.R. Howell |

53,200 | (3) | |

| R.C. King |

48,404 | (4) | |

| P.E. Lippincott |

56,400 | ||

| M.C. Nelson |

68,800 | (5) | |

| S.J. Palmisano |

14,500 | ||

| S.S Reinemund |

13,875 | (6) | |

| W.V. Shipley |

47,040 | ||

| E.E. Whitacre, Jr. |

0 |

| (1) | Includes 10,000 shares held as co-trustee of family foundation. |

| (2) | Includes 5,000 shares owned by spouse. |

| (3) | Includes 5,400 restricted shares held as constructive trustee for former spouse. |

| (4) | Includes 1,000 shares owned by spouse. |

| (5) | Includes 18,000 shares held as co-trustee of family trusts. |

| (6) | Includes 3,375 shares held by family foundation of which Mr. Reinemund is a director. |

On February 29, 2008, ExxonMobil’s incumbent directors and executive officers (27 people) together owned 6,876,891 shares of ExxonMobil stock and 3,577,350 shares covered by exercisable options, representing about 0.20 percent of the outstanding shares.

18

The Compensation Committee of the Board of Directors has reviewed and discussed the “Compensation Discussion and Analysis” for 2007 with management of the Corporation. Based on that review and discussion, we recommended to the Board that the “Compensation Discussion and Analysis” be included in the Corporation’s proxy statement for the 2008 annual meeting of shareholders, and also incorporated by reference in the Corporation’s Annual Report on Form 10-K for the year ended December 31, 2007.

| William R. Howell, Chair | Reatha Clark King | |

| William W. George | Samuel J. Palmisano |

COMPENSATION DISCUSSION AND ANALYSIS

The Compensation Discussion and Analysis and Executive Compensation Tables are organized as follows:

19

Overview

Providing energy to meet the world’s demands is a complex business. We meet this challenge by taking a long-term view rather than reacting to short-term business cycles. The compensation program of ExxonMobil aligns with and supports the long-term business fundamentals and core strategies as outlined below.

| Ÿ | Long investment horizons; |

| Ÿ | Very large capital investments; |

| Ÿ | Worldwide scope of Company operations; and, |

| Ÿ | Commodity-based cyclical market. |

| Ÿ | Long-term growth in shareholder value; |

| Ÿ | Disciplined and long-term focus in making investments; |

| Ÿ | Operational excellence; and, |

| Ÿ | Industry-leading returns on capital and superior cash flow. |

Key Elements of the Compensation Program

The key elements of our compensation program and staffing objectives that support these business fundamentals and strategies are:

| Ÿ | Long-term career orientation with high individual performance standards (see pages 21-22); |

| Ÿ | Base salary that rewards individual experience and performance (see page 22); |

| Ÿ | Annual bonus grants based on business performance, as well as individual experience and performance (see pages 22-23); |

| Ÿ | Payment of a large portion of executive compensation in the form of equity with long mandatory holding periods (see pages 23-24); and, |

| Ÿ | Retirement benefits (pension and savings plans) that provide for financial security after employment (see page 25). |

Other Supporting Compensation and Staffing Principles

| Ÿ | Executives are “at-will” employees of the Company. They do not have employment contracts, a severance program, or any benefits triggered by a change in control. |

| Ÿ | A strong program of management development and succession planning is in place to reinforce a career orientation and provide continuity of internal leadership. |

| Ÿ | All U.S. executives, including the CEO, the other Named Executive Officers, and about 1,200 other U.S. executives, participate in common programs (the same salary, incentive and retirement programs). Within these programs, the compensation of executives is differentiated on the basis of individual experience, level of responsibility, and performance assessment. |

| Ÿ | Substantial amounts of executive compensation are at risk of forfeiture in case of detrimental activity, unapproved early termination, or material negative restatement of financial or operating results. |

20

Business Performance and Basis for Compensation Decisions

| Ÿ | Compensation decisions are based on the results achieved in the following areas over multiple year periods: |

| – | Total shareholder return; |

| – | Net income; |

| – | Return on capital employed; |

| – | Cash returned to shareholders; |

| – | Safety, health, and environmental performance; |

| – | Operating performance of the Upstream, Downstream, and Chemical segments; |

| – | Business controls; and, |

| – | Effective actions that support the long-term, strategic direction of the Company. |

| Ÿ | The decision-making process with respect to compensation requires judgment, taking into account business and individual performance and responsibility. Quantitative targets or formulas are not used to assess individual performance or determine compensation. |

| Ÿ | The disclosure regulations result in a roster of Named Executive Officers different from the most senior management team leading the Company, which is referred to as the Management Committee. |

| Ÿ | The Management Committee comprises the Chairman and CEO (Mr. Tillerson), and three Senior Vice Presidents (Messrs. Albers, Humphreys, and Simon). |

| Ÿ | All members of the Management Committee are shown as Named Executive Officers except for Mr. Albers, who replaced Mr. McGill upon his retirement in 2007. Mr. Albers has short tenure as a Senior Vice President. Consistent with our career orientation, his compensation level does not currently place him among the Named Executive Officers. |

| Ÿ | The three Senior Vice Presidents report directly to the CEO. |

| Ÿ | Although each member of the Management Committee is responsible for specific business activities, together they share responsibility for the performance of the Company. |

Key Elements of the Compensation Program

| Ÿ | It is our objective to attract and retain for a career the best talent available. |

| Ÿ | It takes a long period of time and a significant investment to develop the experienced executive talent necessary to succeed in the oil and gas business; senior executives must have experience with all phases of the business cycle to be effective leaders. |

| Ÿ | Career orientation among a dedicated and highly skilled workforce, combined with the highest performance standards, contributes to the Company’s leadership in the industry and serves the interests of shareholders in the long term. |

| Ÿ | The long Company service of executive officers reflects this strategy at all levels of the organization. |

| – | The Named Executive Officers have career service ranging from 31 to over 42 years. |

| – | The 11 other executive officers of the Corporation have career service ranging from 26 to over 36 years. |

21

| Ÿ | Consistent with our long-term career orientation, high-performing executives typically earn substantially higher levels of compensation in the final years of their careers than in the earlier years. |

| – | This pay practice reinforces the importance of a long-term focus in making decisions that are key to business success. |

| – | Because the compensation program emphasizes individual experience and long-term performance, executives holding similar positions may receive substantially different levels of compensation. |

| Ÿ | Salaries provide executives with a base level of income. |

| Ÿ | The level of annual salary is based on the executive’s responsibility, performance assessment, and career experience. |

| Ÿ | Salary decisions directly affect the level of retirement benefits since salary is included in retirement-benefit formulas. The level of retirement benefits is therefore performance-based like all other elements of compensation. |

| Ÿ | The annual bonus program is highly variable depending on annual financial and operating results. |

| Ÿ | The size of the annual bonus pool is based on the annual net income of the Company and other business performance factors as described beginning on page 28. |

| Ÿ | In setting the size of the annual bonus pool and individual executive awards, the Compensation Committee: |

| – | Secures input from the Chairman on the performance of the Company and from the Compensation Committee’s external consultant regarding compensation trends across industries. |

| – | Uses judgment to manage the overall size of the annual bonus pool taking into consideration the cyclical nature and long-term orientation of the business. |

| Ÿ | The annual bonus program incorporates unique elements to further reinforce retention and recognize performance. Awards under this program are generally delivered as: |

| – | 50 percent cash paid in the year of grant |

| – | 50 percent Earnings Bonus Units with a delayed payout based on earnings performance |

|

Cash

|

+ |

Earnings Bonus Units

|

= |

Annual Bonus

|

| Ÿ | Earnings Bonus Units are cash awards that are tied to future cumulative earnings per share. Earnings Bonus Units pay out when a specified level of cumulative earnings per share is achieved or within three years. |

| – | For bonus awards granted in 2007, the trigger or cumulative earnings per share required for payout of the delayed portion was increased to $5.00 per unit versus $4.25 in 2006, to reinforce the Company’s principle of continuous improvement in business performance and address the impact of the Company’s share repurchase program. |

| – | If cumulative earnings per share do not reach $5.00 within three years, the delayed portion of the bonus would be reduced to an amount equal to the number of units times the actual cumulative earnings per share over the period. |

| – | The intent of the earnings per share trigger is to tie the timing of the bonus payment, not the amount, to the rate of the Corporation’s future earnings. Thus, the trigger of $5.00 is intentionally set at a level that is expected to be achieved within the three-year period. |

22

| – | Prior to payment, the delayed portion of a bonus may be forfeited if the executive leaves the Company before the standard retirement age, or engages in activity that is detrimental to the Company. |

| – | Cash and Earnings Bonus Unit payments are subject to recoupment in the event of material negative restatement of the Corporation’s reported financial or operating results. Recoupment guidelines approved by the Board of Directors are described on page 32. |

| Ÿ | The 2007 annual bonus pool was $214 million versus $217 million in 2006. This reflects the combined value at grant of cash and Earnings Bonus Units. |

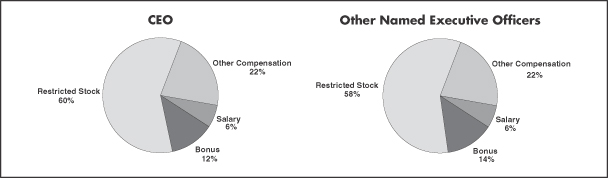

| Ÿ | Equity compensation accounts for a substantial portion of total compensation to align the personal financial interests of executives with the long-term interests of shareholders. |

| Ÿ | It is the objective to grant 50 to 70 percent of a senior executive’s total compensation in the form of restricted stock, as described on page 31. |

Rationale

| Ÿ | Given the long-term orientation of our business, granting equity in the form of restricted stock with long vesting provisions keeps executives focused on the fundamental premise that decisions made currently affect the performance of the Corporation and Company stock many years into the future. |

| Ÿ | This practice supports a risk/reward profile that reinforces a long-term view, which is fundamental to the business. |

| Ÿ | Restricted stock removes employee discretion on the sale of Company-granted stock holdings and reinforces the retention objectives of the compensation program. |

Restriction Periods

| Ÿ | The restricted periods for ExxonMobil’s stock grants are longer than those used by most other large companies. For the most senior executives: |

| – | 50 percent of each grant is restricted for five years; and, |

| – | The balance is restricted for 10 years or until retirement, whichever is later. |

| Ÿ | The long restriction periods: |

| – | Align with the Company’s focus on growing shareholder value over the long term; and, |

| – | Make a large percentage of executive compensation and personal net worth subject to the return on ExxonMobil stock realized by shareholders. |

| Ÿ | For the most senior executives, more than half of the total amount of restricted stock may not be sold or transferred until after the executive retires. |

| Ÿ | The restricted period for stock awards is not subject to acceleration, except in the case of death. |

Forfeiture Risk and Hedging Policy

| Ÿ | Restricted stock is subject to forfeiture if an executive: |

| – | Leaves the Company before standard retirement time (defined as age 65 for U.S. employees). In the event of early retirement prior to the age of 65 (i.e., age 55 to 64), the Compensation Committee must approve the retention of awards by an executive officer. |

| – | Engages in activity that is detrimental to the Company, even if such activity occurs or is discovered after retirement. |

23

| Ÿ | Company policy prohibits executives from entering into put or call options that might be used to hedge an executive’s financial exposure to ExxonMobil common stock. |

Share Utilization

| Ÿ | The Compensation Committee establishes a ceiling each year for annual stock awards. The overall number of shares granted in the restricted stock program in 2007 represents dilution of less than 0.2 percent, which is well below the average of the other large U.S.-based companies that are benchmarked for compensation and incentive program purposes based on their historical grant patterns. |

| Ÿ | The Company has a long established practice of purchasing shares in the marketplace to eliminate the dilutive effect of stock-based incentive awards. |

Prior Stock Programs

| Ÿ | All equity awards granted since 2003 are granted under the Corporation’s 2003 Incentive Program. All equity-based awards (including stock options and restricted stock) granted prior to 2003 that remain outstanding were granted under the Corporation’s 1993 Incentive Program (other than awards granted by Mobil Corporation prior to the merger). No further grants can be made under the 1993 Incentive Program. |

| Ÿ | Prior to 2002, ExxonMobil granted Career Shares to the Company’s most senior executives. |

| – | Career Shares, which do not vest until the year following an executive’s retirement and are subject to forfeiture on substantially the same terms as current grants of restricted stock, further align the personal financial interests of executives with the long-term interests of shareholders and help ExxonMobil retain senior executives for the duration of their careers. |

| – | The Corporation ceased granting Career Shares in 2002 when the Corporation began granting restricted stock to the broader executive population in lieu of stock options. |

| – | Restricted stock and long mandatory holding periods achieve the same objectives as Career Shares, and therefore it is unnecessary to grant both Career Shares and the current form of restricted stock. |

| – | Career Shares could be granted again in the future under the Corporation’s 2003 Incentive Program, but there are no current plans to make such grants. |

Stock Ownership